by Joe Herrle, CFA

Senior Vice President

Alternative Assets and Portfolio Management

Although we appreciate access to a wealth of data in our offices, a site visit no doubt provides a more holistic perspective for us.

Our team recently spent a morning touring a sprawling data center campus in Hillsboro, Oregon. Even for a group that follows this industry closely, the scale was staggering. The roughly 90-acre site is split into five mega-facilities, more than a million square feet of computing space drawing over 250 megawatts of power, that could supply a small city. Walking the floors, we came away with a clearer picture of what these buildings actually do, with several of our long-held misconceptions corrected.

At its simplest, a data center is a heavily secured warehouse for computers. Rows of servers store the photos, emails, financial records and streaming videos we rely on every day and increasingly the artificial intelligence models reshaping how we work. When you send a text, check a balance, or ask a chatbot a question, a building like this one does the work. The “cloud”—simply computing and storage delivered over the internet rather than from your own device—is not abstract. It is concrete, steel and silicon humming away in places like Hillsboro.

Two Myths Worth Correcting

The first myth is water. Headlines often describe data centers as draining local water supplies for cooling. The campus we visited uses none; it relies on a closed, air-based cooling system that places no strain on the region’s water. The second myth is the grid. Critics argue that these facilities only consume electricity and push up rates for everyone else. This site is moving in the opposite direction: it plans to generate its own power on-site, paired with large-scale battery storage, and to feed electricity back to the grid at peak demand—a design that can stabilize and possibly lower local energy prices.

A Wider Economic Footprint

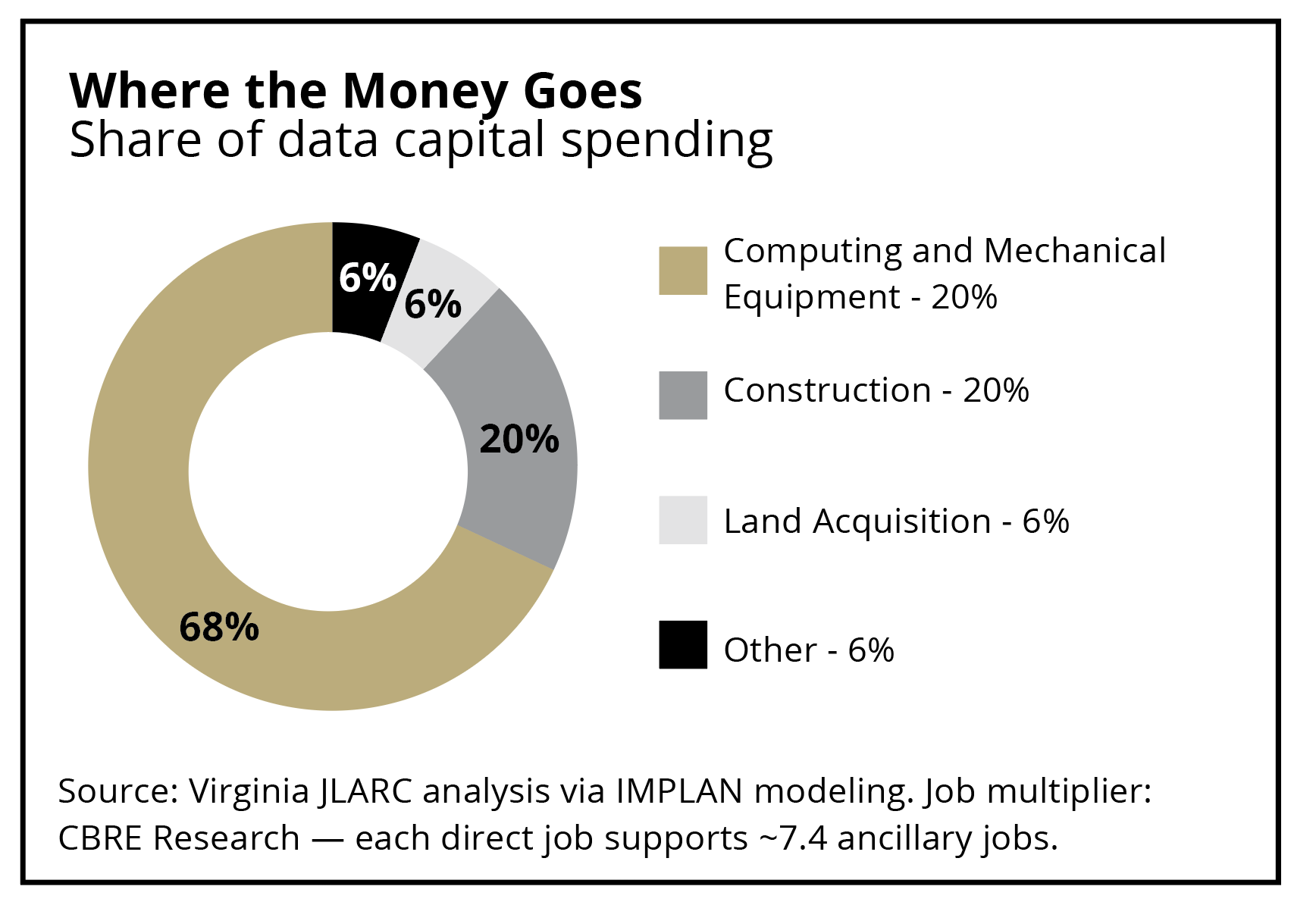

The economic impact reaches well beyond the fence line. Building one of these campuses is enormously capital-intensive, and most of that money flows outward. Roughly two-thirds of the spend goes to computing and mechanical equipment (chips, servers, transformers and cooling systems), supporting semiconductor, electrical and manufacturing firms nationwide. Power utilities, fiber and networking providers, and real-estate developers benefit as well. An additional one-fifth funds construction, employing local tradespeople for years. The ripple is substantial: industry research estimates that each direct data center job supports more than seven additional jobs across the wider economy, from electricians and HVAC technicians, to truck drivers and restaurant staff. The facilities also have become major local taxpayers, helping fund schools, roads and public services.

A Catalyst for an Energy Renaissance

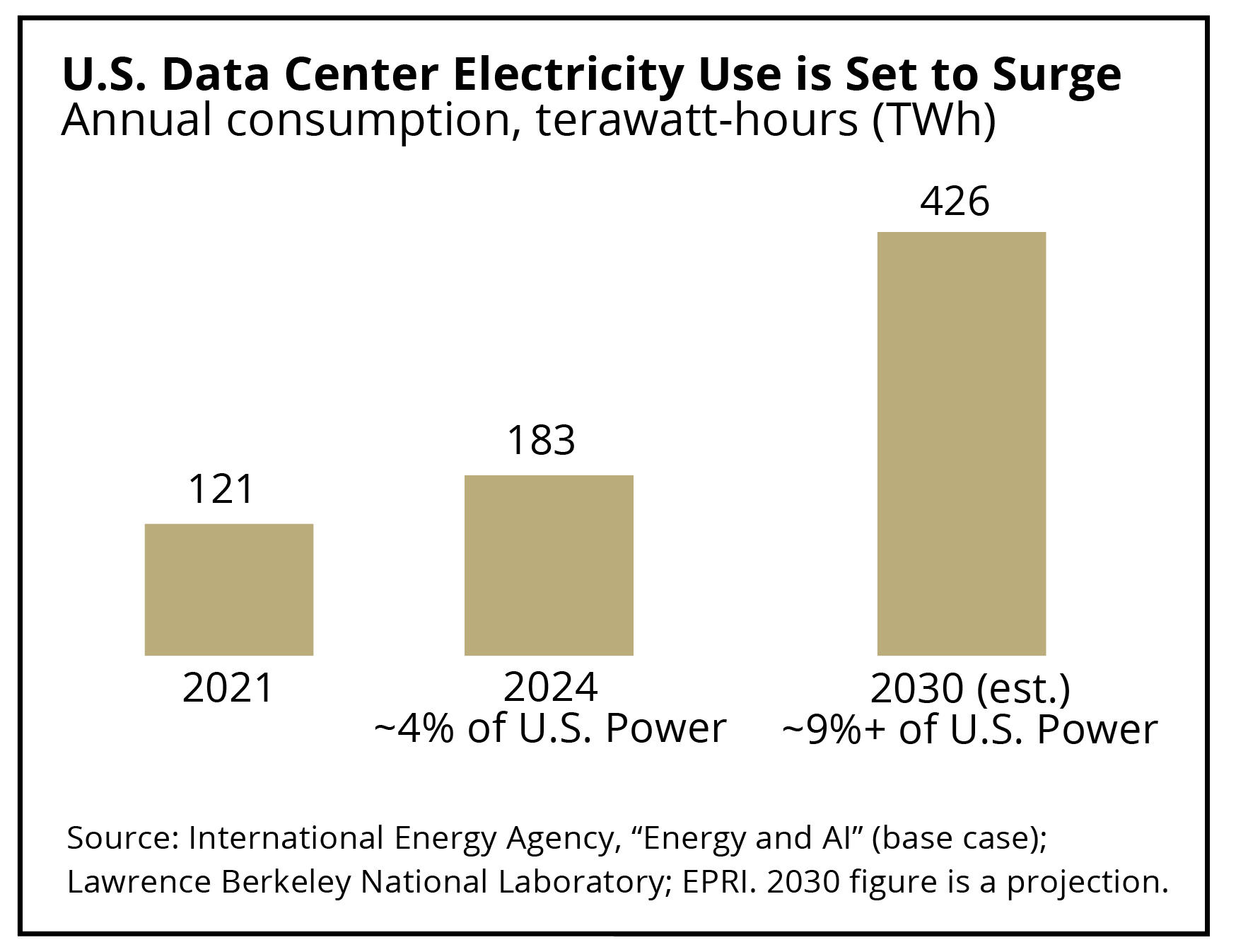

Perhaps the most consequential effect is on energy itself. U.S. data centers consumed roughly 4% of the nation’s electricity in 2024, and that share is expected to more than double by 2030 as AI scales. Rather than a strain, this demand is becoming a catalyst for an energy renaissance. To power these facilities reliably and cleanly, technology companies are funding new natural gas, advanced nuclear (including small modular reactors), geothermal, solar and grid-scale battery projects. These investments that may ultimately benefit all electricity users, not just data centers.

This matters beyond any balance sheet. Few inputs are as closely tied to human well-being as affordable, abundant energy. Reliable, low-cost power raises living standards, lowers the cost of goods and widens access to healthcare, education and opportunity. If the AI build-out accelerates innovation in how we generate and store electricity, the benefits could reach far beyond the server racks.

None of this is lost on us as investors. Data centers and the broader ecosystem around them, such as equipment makers, power producers, utilities and infrastructure owners, sit at the center of a multi-year capital cycle. For that reason, this theme is a core thesis within our equity and alternative-asset strategies, and one we will continue to follow closely on your behalf.

Disclosures

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.