George Hosfield, CFA

Chief Investment Officer

Director

At the close of the first quarter, the capital markets were digesting an array of economic shocks. Geopolitical tensions in the Middle East, rising energy costs and shifting expectations regarding Federal Reserve policy all contributed to the pullback in stocks. Additionally, early fears regarding artificial intelligence (AI) displacing traditional technology roles triggered a significant selloff in software equities. However, as the second quarter progressed, the market shifted its sights from the near-term economic risks associated with oil-driven inflation, to the substantial earnings potential currently being generated by the investments in AI infrastructure ... particularly benefiting semiconductor companies.

AI Investment is Propelling Economic Growth

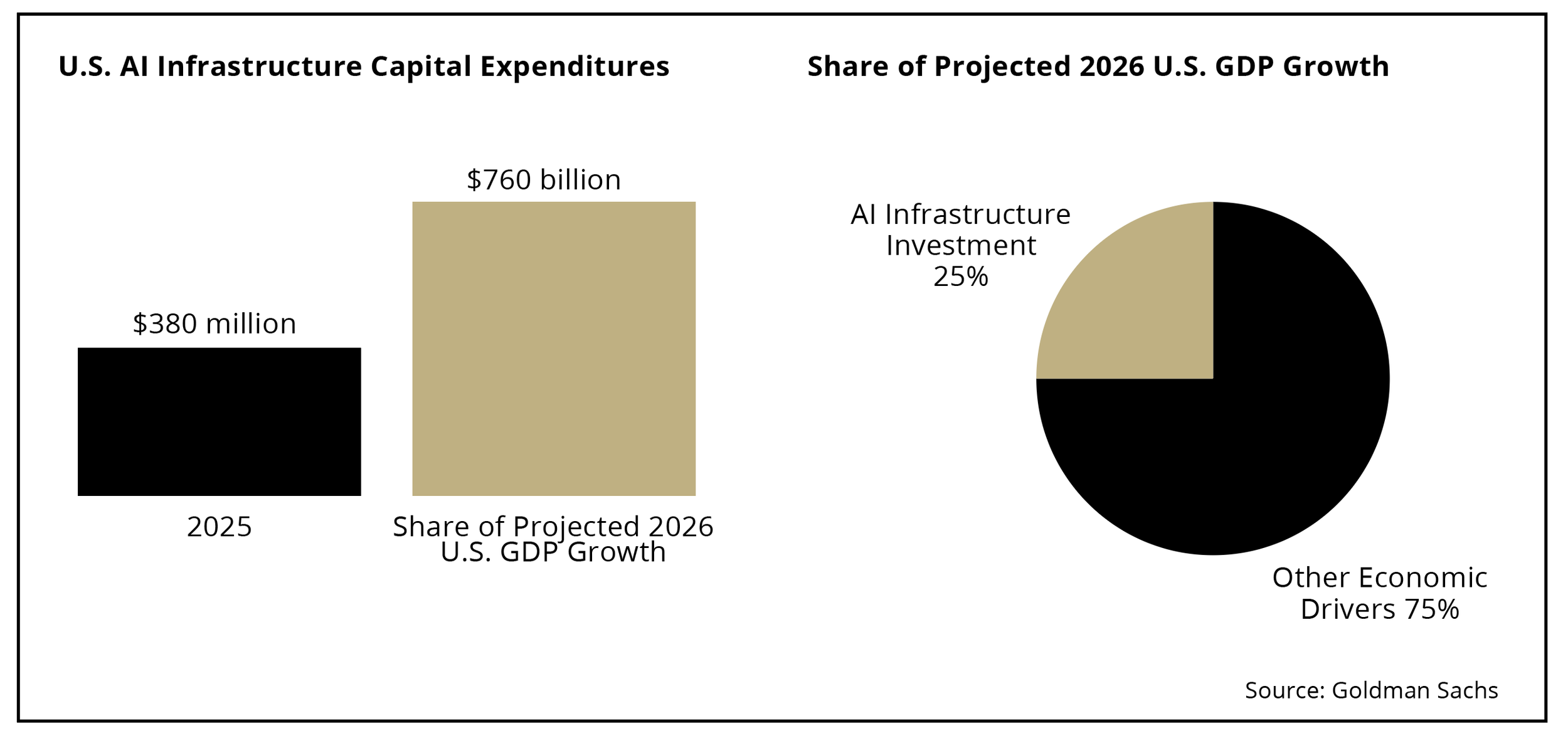

The sheer scale of capital currently being allocated to AI is acting as a powerful tailwind for the broader economy. U.S. AI infrastructure capital expenditures are projected to double over the next year, increasing from $380 billion in 2025 to $760 billion in 2026. While this specific infrastructure investment represents only 12% of total U.S. gross domestic product, this investment will be an outsized contributor to the trajectory of the economy as it will account for 25% of the projected economic growth for all of 2026. In round numbers, consumer spending is expected to make up 50% of 2026 economic growth, while government spending and other capital investments are expected to account for the remaining 25%.

Supported by these drivers, U.S. economic data continues to surprise to the upside. With unemployment at only 4.3% and payroll growth ahead of expectations, the labor market has improved compared to the second half of 2025. Furthermore, as a result of the capital spending required to build data centers, power generation and networking equipment for this “AI supercycle,” manufacturing indicators have begun to turn higher after a prolonged period of weakness.

Earnings Estimates are Surging

This economic backdrop has led to steady and significant upward revisions for corporate profitability. Specifically, propelled by the technology and energy sectors, S&P 500 earnings growth estimates for 2026 have ballooned from 15% at the beginning of the year to 25% today. It is important to note that recent stock market gains have been fundamentally supported by underlying business performance rather than mere speculation. To that end, from a valuation standpoint, while the S&P 500 has enjoyed a return approaching double digits through the first half of the year, because corporate earnings are growing at a faster pace than price appreciation, the market valuation (e.g., price/ earnings ratio) has actually contracted, resulting in a market that is 9% cheaper today than it was at the start of the year.

The AI Job Market Reality

Despite the early concerns that rattled software stocks in the first quarter, so far employment data indicates that AI is not eliminating software engineering roles on a net basis. On the contrary, software developer job postings have accelerated higher over the last few months, a trend that aligns directly with the overall increase in AI investment. As the practical applications and viability of AI as a revolutionary technology become clearer, companies recognize that human developers are strictly necessary. These professionals are required to validate, implement and secure the vast amounts of code generated by AI models, leading to job growth in the sector rather than workforce reduction.

Inflation and Interest Rates

While our outlook for the economy continues to be positive, inflation remains the key risk to our constructive thesis. Specifically, oil prices have pushed headline inflation higher in recent months, culminating in the May headline inflation reaching 4.2%. We recognize that sustained inflation above the 4% threshold presents tangible economic risks, including the erosion of consumer purchasing power, valuation compression for equities and the necessity for higher borrowing costs. However, at this juncture, we expect the near-term inflationary pressures driven by energy markets to moderate, and we anticipate inflation will settle between 3.5% and 4.0% by year-end. Though moderating, this level of inflation, combined with better-than-expected economic growth, supports the likelihood that interest rates will remain higher for longer as the Federal Reserve will likely place a priority on maintaining price stability.

Client Portfolios

Reflecting our confidence in the current economic environment, we have made modest, yet deliberate adjustments to client portfolios to align with these macroeconomic trends. Given the combination of strong economic growth and higher inflation, we reduced our exposure to defensive, interest rate sensitive sectors, specifically trimming our allocations to utilities and consumer staples. Conversely, the ongoing strength and visibility in AI capital spending prompted us to increase our exposure to technology and basic materials as these industries are positioned to benefit from providing the resources and raw materials, that are essential for the multi-year AI infrastructure build out.

Disclosures

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.