Samantha Pahlow, CTFA, AWMA

Wealth Management Chair

Investors often focus on what they own and how those investments may perform, paying less attention to where assets are held and who stands behind them. Past events, including the very different failures of FTX (2022) and Silicon Valley Bank (2023), have made those questions more tangible. If something goes wrong with the institution holding your assets, what happens next?

A common misconception is that money “in” a brokerage account works the same way as money “in” a bank account. It does not. The two arrangements differ in how your assets are held, who has a claim on them and what protections apply if the institution fails.

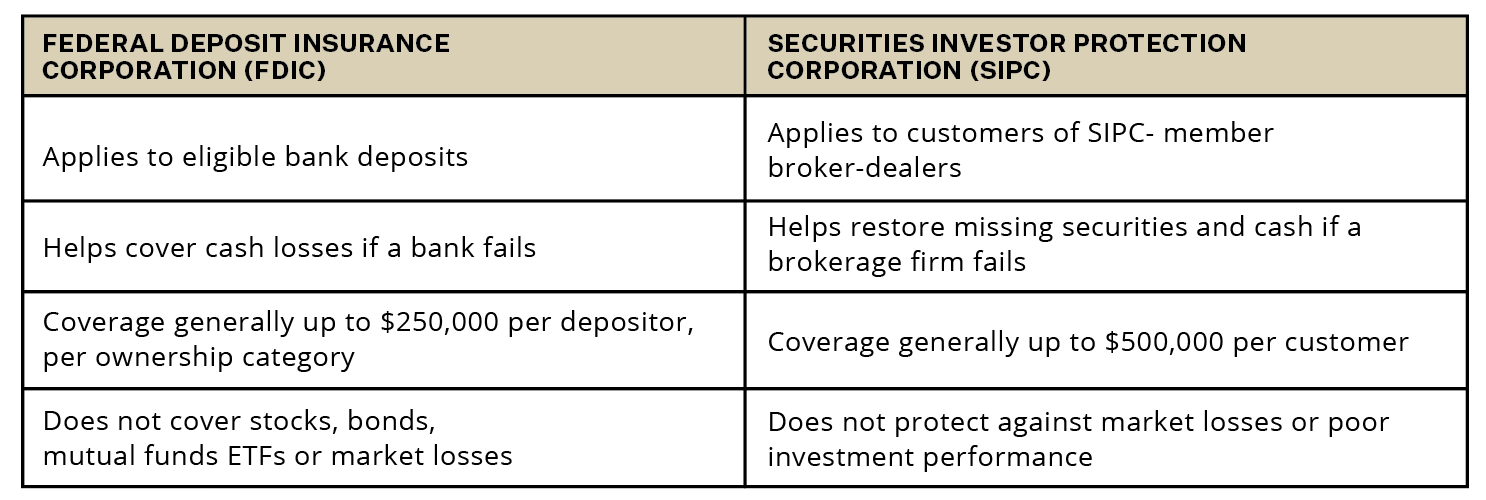

Banks and FDIC Coverage

When you deposit cash at a bank, the bank uses that money to make loans and conduct other activities, owing you the balance back and often paying interest. In effect, you are a creditor of the bank. If the bank fails, balances above applicable insurance limits may be at risk.

This is where Federal Deposit Insurance Corporation (FDIC) insurance comes in. It covers eligible deposits at FDIC-insured institutions up to $250,000 per depositor, per insured bank, for each ownership category. It does not cover investment losses or securities.

For most depositors, this is low risk. Still, for balances well above the limits, it may help to review the location and titling of your cash. Because limits apply per depositor, per ownership category, titling can multiply coverage. A married couple, for example, may be able to qualify for $1 million of coverage at one FDIC-insured bank through properly titled individual and joint accounts, assuming they have no other deposits at that bank in the same ownership categories. Coverage limits and ownership-category rules can be complex; individuals should consult with their financial professionals regarding their specific circumstances.

Brokerage Accounts and SIPC Protection

A brokerage account is structured differently. When you hold securities—stocks, bonds, mutual funds or exchange-traded funds (ETFs)—in a brokerage account, those assets are generally held for your benefit by the brokerage firm or custodian. The custodian provides safekeeping, recordkeeping, trade settlement and reporting, but fully paid securities are generally required to be kept separate from the custodian’s own assets. In the event of a custodian failure, if assets have been properly maintained, they continue to be the property of the investor and could be transferred to a new custodian.

Securities Investor Protection Corporation (SIPC) protection applies when a SIPC-member brokerage firm fails, and customer securities or cash are missing. Coverage is limited to $500,000 per customer, including up to $250,000 for cash held for the purpose of purchasing securities. Many large custodians also carry additional private insurance, often referred to as “excess SIPC,” which may extend protection beyond statutory SIPC limits, subject to program terms, aggregate limits and exclusions. SIPC does not protect against market declines, unsuitable investments, bad advice or assets held outside a SIPC-member brokerage firm.

Ferguson Wellman is an investment adviser, not a custodian. Our clients’ assets are primarily held at Charles Schwab, an independent qualified custodian, in accounts titled in the client’s name. As of this writing, Schwab states that its combined SIPC and excess SIPC coverage provides protection up to an aggregate program limit of $600 million. This is limited to a combined return of $150 million per customer, including up to $1.15 million in cash. Coverage is subject to program terms and does not protect against market losses. Where assets are custodied elsewhere, your portfolio manager or client relationship associate can help answer questions about applicable coverage.

A Note on Assets Held Outside Traditional Custody

Exercise caution with assets held outside traditional bank or brokerage custody. If an investment is held outside a qualified custodian—for example, certain private investments, crypto platforms or a promissory note from private issuers—it’s possible that neither the FDIC nor SIPC protections described below will apply. That does not necessarily make the investment inappropriate, but it changes the risk profile and warrants additional due diligence.

Putting It Together

Custody arrangements, account titles and insurance coverage may not be visible day-to-day, but they are important parts of your wealth architecture. Established protections—including FDIC insurance, SIPC protection, SEC custody rules for advisers and customer protection rules for broker-dealers—are designed to provide meaningful safeguards. These protections, however, are not interchangeable and do not cover every type of risk. Understanding how they work can help you make more informed decisions about where and how your assets are held.

Disclosures

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.