by Brad Houle, CFA

Principal

Head of Fixed Income

Portfolio Management

Private credit has become one of the fastest growing segments of global capital markets. Once viewed as a niche alternative investment strategy, it has evolved into a significant source of financing for small and middle market companies.

As assets have flowed into the sector, recent headlines about redemption restrictions, or "gates," at several large private credit funds have raised questions among investors. Understanding what private credit is, why it has grown so rapidly, and what gating actually means can help distinguish normal market evolution from genuine cause for concern.

At its core, private credit refers to loans made directly to businesses by investment funds rather than through traditional banks or public bond markets. These loans are typically negotiated privately, allowing lenders and borrowers to structure terms that meet their specific needs. Often, companies are able to get more flexible terms by not using public markets to borrow. Unlike publicly traded bonds, private credit investments are generally not bought and sold in active secondary markets.

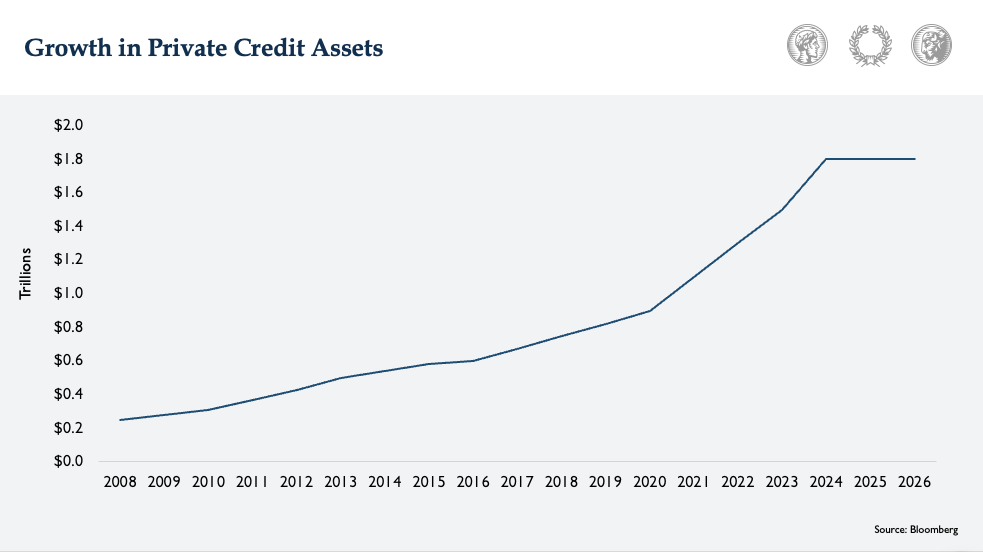

The asset class expanded dramatically following the Global Financial Crisis (GFC). Increased banking regulation reduced the willingness and ability of traditional banks to lend to many middle-market companies. Private credit managers stepped in to fill the gap, providing borrowers with faster execution, greater flexibility and customized financing solutions. Additionally, the period following the GFC saw a protracted period of low interest rates and investors seeking higher yields flocked to the asset class. The growth has been remarkable, with estimates placing the size of the private credit market between $1.5 trillion and $2 trillion, a size comparable to the public high yield debt markets.

The sector is now facing its first meaningful test. Following years of rapid growth and intense competition among lenders, underwriting standards in some areas have weakened and loan spreads have compressed. Loans to certain industries, such as software, are beginning to show signs of stress.

That said, current conditions do not resemble a broad credit crisis. Default rates remain manageable across much of the industry, and most managers continue to report stable portfolio performance. Currently, the actual default rate is very low at around 1% to 3% with “selective defaults”, a restructuring of loan terms that is around 5% (Bloomberg). What we are seeing appears to be less of a systemic breakdown and more of a transition from an era of abundant capital to one where credit selection and underwriting discipline matter more. If we go into an actual recession (which we are not currently anticipating) the default rate will climb much higher. This, however, is not an issue that is likely to become a systemic problem for the financial system and create broad stress in the banking system like we saw in 2008 with residential mortgages.

Recently, attention has focused on redemption gates implemented by several large private credit funds. While the headlines can sound alarming, gating is not necessarily evidence of deteriorating credit quality.

Private credit investments are inherently illiquid. The underlying loans cannot be sold quickly without potentially accepting significant discounts. Yet many credit funds offer periodic liquidity to investors. Gates exist to manage this mismatch.

Most funds limit quarterly redemptions to a predetermined percentage of net asset value, often around 5%. When redemption requests exceed that amount, withdrawals are fulfilled over multiple periods rather than immediately.

These mechanisms serve several important purposes. They help prevent forced asset sales, reduce the risk of investor runs, preserve portfolio value and ensure fair treatment among shareholders. In many respects, gates are functioning exactly as designed.

As the market matures, the distinction between strong and weak managers is likely to become more apparent. The next phase of private credit will be driven less by asset growth and more by underwriting quality, credit expertise and disciplined risk management.

Takeaways for the Week

The higher yields associated with private credit are, in part, compensation for accepting reduced liquidity. Gating is necessary to allow for orderly liquidity.

We don’t currently view this weakness in private credit to be a potential systemic issue for the financial system.

Disclosure

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.