by Blaine Dickason

Senior Vice President

Portfolio Management and Trading

After spending the last 36 years in Pioneer Tower, this week, we moved into our new Portland office location just two blocks away in Fox Tower. This comes with significantly different views, and while the view out our window has changed, the economic landscape and investing environment we work in took scant notice of our change of address. A similar dynamic played out at the Federal Reserve this month, where the views have also changed, in their case from new leadership, yet the environment and challenges they’re facing remain the same.

Federal Reserve Chair Kevin Warsh, sworn in last Friday, begins his term having already expressed new ideas that would shift how the Fed conducts its monetary policy. What hasn’t changed, however, is the current inflation running above the Fed’s self-declared 2% target, where it has lived for over 5 years. A major question for financial markets as Warsh begins his term as chair is whether his new perspectives and ideas for shifting Fed policy will be more effective at returning inflation to target than previous Chair Jerome Powell’s. At the same time, Warsh can’t lose sight of maintaining maximum employment, the other tenet of the Fed’s dual mandate. Another open question is whether any single new individual at the helm of this institution will be able to implement many new ideas in a policy-setting body comprised of six other Fed governors and 12 regional bank presidents. Given this structure, his call for “regime change” at the Fed during one of his pre-confirmation hearings may not be as easy to accomplish as he might like.

The bond market may have already done Chair Warsh a favor as yields have trended higher this year, largely in response to the energy shock and the feared inflationary effects from higher oil prices. In other words, the bond market may have done the Fed’s job for it already, as higher yields set by the market will be viewed as more restrictive, and may obviate the need for a possible interest rate hike before year-end.

Ceasefire Optimism

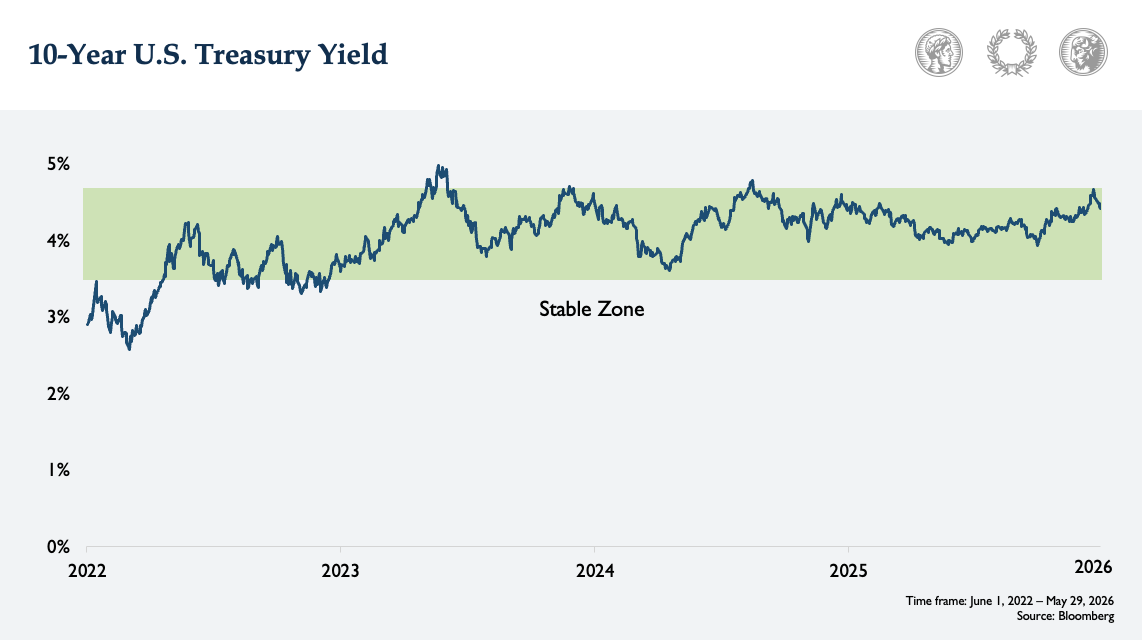

While continued positive momentum in corporate earnings has been the backbone of the S&P 500’s performance this year, other corners of the financial markets are continuing to express cautious optimism towards a ceasefire or major deescalation of the war in Iran. Most notably this week, the yield on the 10-year U.S. Treasury declined back below 4.5% after testing the upper bound of our unofficial ‘stable zone’ earlier in the month (chart below), which might have signaled graver concern about lasting inflationary pressures or funding the U.S. government. Additionally, commodity markets are now expecting the price of West Texas Intermediate (WTI) crude oil for delivery in December to return to below $80 per barrel. Both these moves are indications the financial markets are looking ahead to a resumption of the oil supply through the Strait of Hormuz and a reduction in the inflationary pressures from the energy shock.

Takeaways for the Week:

The S&P 500 posted its 9th straight week of gains and returned over 5% for the month of May

Yesterday, the Federal Reserve Bank of Atlanta’s GDPNow model estimate indicated the U.S. economy (GDP) is growing at an annual rate of 3.8% so far in the second quarter

Disclosure: The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional Disclosures.