by Chris Bixby, CFP®, EA

Senior Vice President

Portfolio and Wealth Management

The 2026 Washington State Legislative Session was quite active for a short 60-day session. Despite the short session, multiple changes were made regarding the Business & Occupation tax, Sales tax, Estate tax, and Capital Gains tax. These were largely overshadowed by the passing of a state income tax, commonly referred to as the “Millionaires’ Tax”.

For many, the “Millionaires’ Tax” created more questions than answers; questions that will need to be addressed during the next legislative session. Additionally, court challenges and a possible referendum vote leave the enactment of this law in limbo. What we do know is that the law, as it currently stands, imposes a 9.9% tax on incomes over $1 million, beginning in 2028. As the panorama around this tax clears, we will come back with more information. More pertinent are the changes to the Estate tax and Capital Gains tax, which we will discuss below.

Capital Gains Tax

The WA Capital Gains tax imposes a 7% tax on capital gains over $278,000, adjusted for inflation. Largely, these taxes follow the capital gains calculations on the federal tax return, with notable exceptions for real estate and farming. However, new in 2026, but retroactive to 2025, is a new graduated range. For taxable gains over $1,000,000, an additional 2.9% surtax is applied.

Example: Taxpayer has $2,000,000 of capital gains on their 2025 federal tax return. The WA Capital Gains tax is applied to $1,722,000 ($2,000,000 - $278,000). The first $1,000,000 will be taxed at 7%, while the remaining $722,000 will be taxed at 9.9%. This results in a total tax of $141,478. ($1,000,000 x 7% = $70,000. $722,000 x 9.9% = $71,478. $70,000 + $71,478 = $141,478).

Also new in 2026 is a credit for Business & Occupation taxes paid on property that generates a capital gain. In addition, a proposal to tax gains generated by the sale of Qualified Small Business Stock, which is non-taxable at the federal level, was deferred until the next session. This proposal should be carefully followed by anyone expecting to sell a qualifying small business in the next few years.

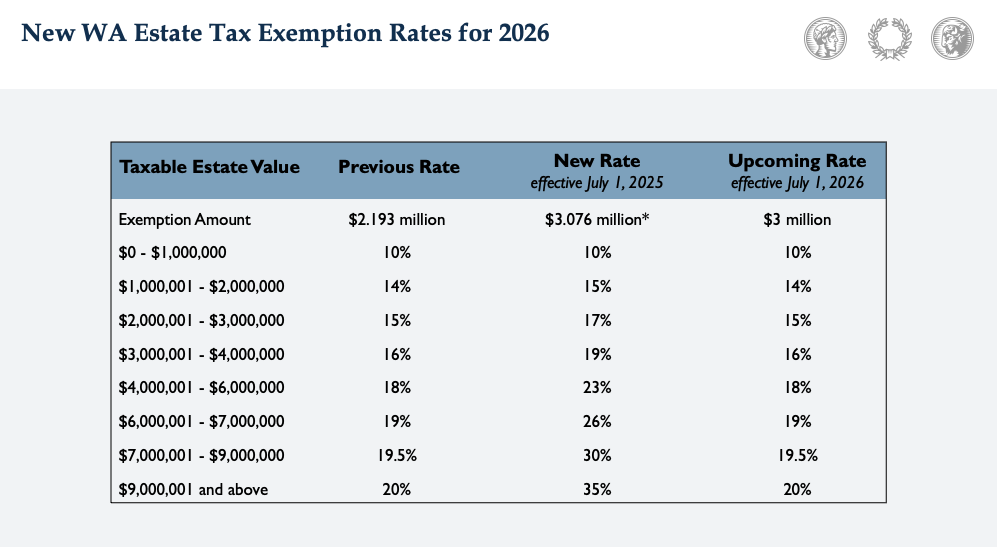

Estate Tax

In 2025, the WA State Legislature passed an increase to the estate tax. The maximum rate increased from 20% to 35%, making Washington the state with the highest estate tax rate in the nation. The 2026 Legislative Session reversed course, re-instating 20% as the highest tax rate. The rules are complex and subject to interpretation as well as potential revisions. However, there are a few important nuances that need to be understood.

The first nuance is that the new rates do not become effective until July 1, 2026, meaning that there are two different tax rates for the 2026 tax year. The table below shows the changing impact of the tax rates as well as the exemption amount. Note that the exemption amount has been set at $3 million, meaning that any taxpayer who passes away with less than $3 million in total assets is not subject to the tax.

One other note of interest is that the 2025 Legislative Session increased the exemption to $3 million and indexed the exemption by inflation. For estates starting in 2026, the amount of the inflation-adjusted index was $3.076 million. The 2026 Legislative Session reset the indexed amount and included future index language but pointed to an index that does not formally exist. This may be an oversight that will be corrected during the next session.

*This is the inflation adjusted number for deaths occurring between 1/1/2026 and 6/30/2026. Estates for decedents with a date of death from 7/1/2025 to 12/31/2025 were subject to a $3,000,000 exemption.

Conclusion

As with all tax matters, using your team of advisors is essential to arrive at a desired outcome. These tax law changes are significant, and planning carefully for the future can, in many cases, help to mitigate these taxes. However, tax law changes should always be considered in light of your goals and objectives, not as a standalone decision-making item.

Please consult with your portfolio manager and tax and legal advisors should you want to study how these changes affect you personally.

Disclosure

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.