Krystal Daibes Higgins, CFA

Senior Vice President

Equity Research and Portfolio Management

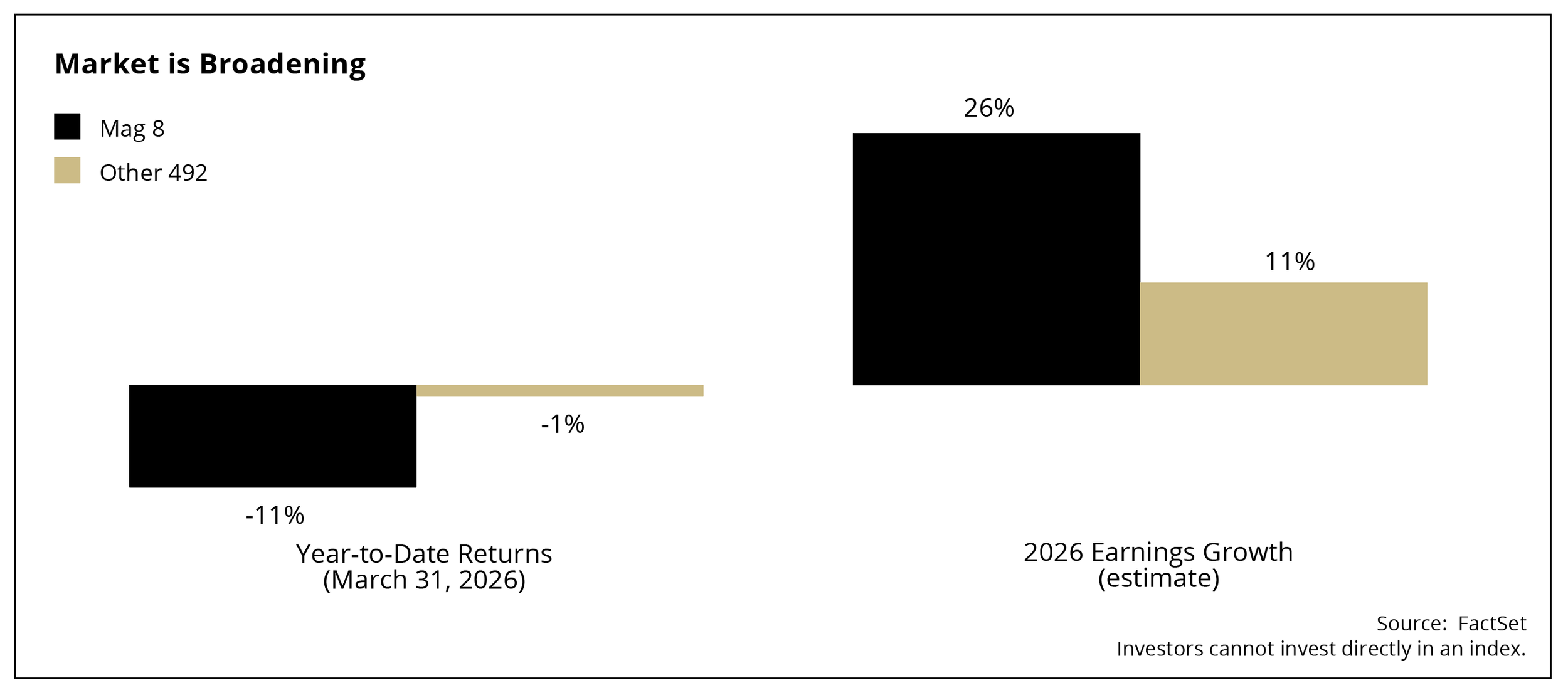

Software stocks have experienced a selloff of over 30% since October 2025, largely driven by uncertainty around the competitive risks of artificial intelligence (AI). While AI will have a significant impact on software companies, the more relevant question for investors is understanding if it is an opportunity or a risk for individual businesses. Our investment approach when assessing technology stocks continues to center on three key attributes: durable earnings growth, financial strength (reflected in healthy balance sheets and cash flow generation) and, importantly, a company’s ability to navigate and innovate in ways that remain essential to its customers. These characteristics are increasingly defining the separation of category leaders from less differentiated players. However, more recently the emphasis investors are placing on each has changed.

Growth, the primary driver of valuation for much of the past cycle, while necessary, is no longer sufficient on its own. In addition, investors are placing greater weight on the durability of demand over a multi-year horizon without having to re-invest a large amount of capital from operating cash flows and, worse, debt.

The shift is evident in the dispersion across the technology landscape. As of late, businesses with blowout earnings growth, strong net customer retention, resilient and/or expanding margins and improving cash flow are no longer being rewarded in the same way they once were. Some that have far surpassed expectations saw their stock prices fall as investors failed to reward them for planning to reinvest in future growth. As a result, a number of high-quality growth companies that delivered exceptional performance over the past few years have seen their valuations compress.

This reset reflects a shift in investor psychology. There is a tendency to assume that periods of strong growth are unsustainable, leading to profit-taking even when underlying long-term fundamentals remain intact.

While a degree of skepticism is always warranted, we believe the market may be underestimating the durability of growth for a subset of these businesses. The current repricing may create a better entry point, particularly within software, where long-term demand drivers remain firmly in place.

It is also worth noting that in periods of elevated volatility, management guidance is often met with increased scrutiny. In our experience, leadership teams at large, leading global companies tend to have a clearer line of sight into their demand environment than the market assumes. While not infallible, their track record of navigating prior cycles often suggests they are better than Wall Street estimates.

In our opinion, this environment creates a more favorable backdrop for individual stock selection. Periods of indiscriminate selling often obscure fundamental differences between businesses, allowing high-quality companies to be purchased at more reasonable valuations.

Market volatility tends to feel most acute in realtime. However, it serves as an important function by resetting expectations and aligning valuations with fundamentals when optimism or pessimism is overdone.

This is where discipline matters most. As expectations reset and valuations adjust, the opportunity set improves. The focus should remain on owning resilient businesses with durable growth, where temporary price dislocations may create a more compelling entry point for long-term investors.

Disclosure

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.