George Hosfield, CFA

Chief Investment Officer

Director

In the first quarter, several market-disrupting events took place: the Supreme Court struck down International Emergency Economic Powers Act (IEEPA) tariffs, war began in the Middle East, oil prices rose over 70%, expectations for two Federal Reserve rate cuts evaporated and AI substitution fears triggered a 20% selloff in software stocks, the S&P 500’s second-largest industry. While none of these are positive developments for the capital markets, the fact that the S&P 500 is only down 4% year-to-date suggests the economic fallout may be much less than the current headlines suggest (as of March 31, 2026). To provide some perspective, we offer the following context:

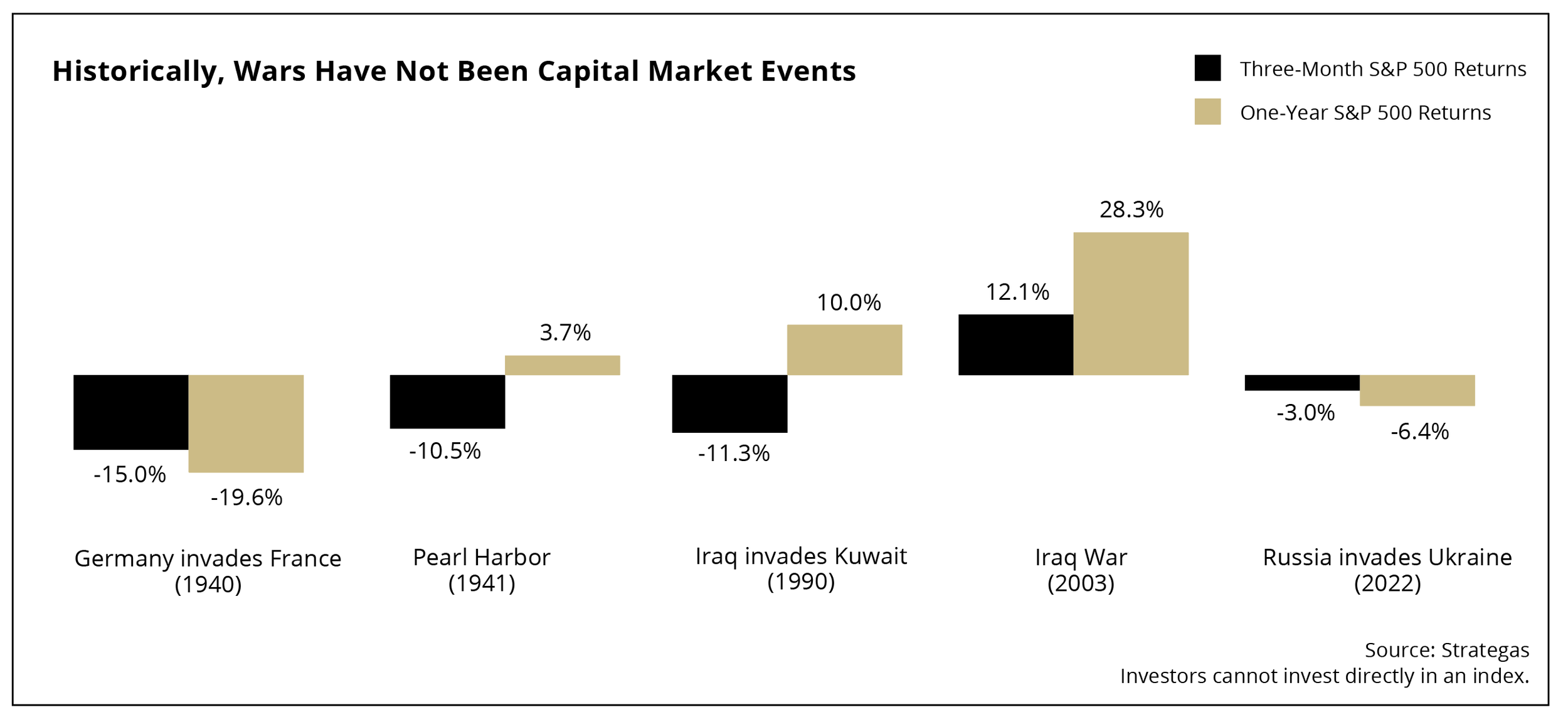

War in the Middle East: Historically, wars have not been sustained capital market events. As can be seen in the accompanying graph, the initial market reaction is often to sell risk assets in the first few months after hostilities begin. Ultimately, the underlying economy and corporate earnings dictate the direction of equity markets. Case in point: sadly, the war in Ukraine is now in its fourth year, yet the S&P 500 has enjoyed three consecutive years of double-digit returns. With the current war in Iran, the key economic risk is a sustained increase in oil prices, which would lead to both inflation and an economic slowdown. It is too early to see any real impact, yet investors are handicapping a short-term spike, rather than long-term higher prices.

Tariffs: Though the effective tariff regime is now lower than it was prior to the Supreme Court ruling, this has been a decidedly negative development because the hope was that businesses by now would have visibility into the “rules of the game.” However, the removal of IEEPA tariffs plunged global trade back into uncertainty, as the administration is looking to use other means to keep tariff rates high. Unfortunately, we believe this uncertainty has affected businesses’ hiring decisions, with hiring remaining anemic.

Gas Prices: Americans spent only 3.5% of their income on all types of energy in 2025: with gasoline comprising less than half of that. To give a sense of consumer sensitivity, when oil peaked at $115/barrel in 2022, energy expenditures were 5% of income. In other words, the increased price of gas has a greater emotional impact on consumers than on their budgets.

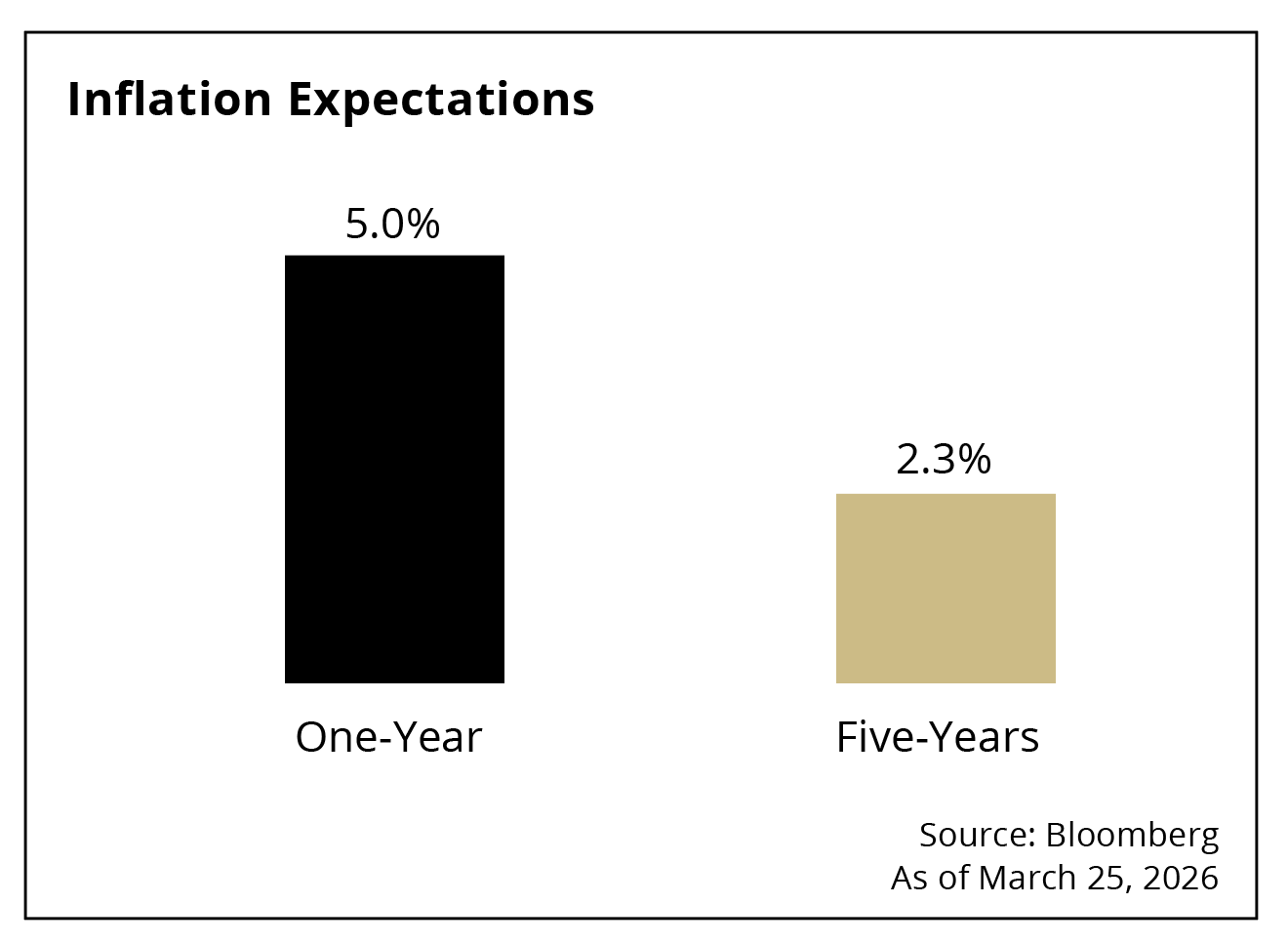

The Impact of Higher Gas Prices on Inflation

The inflation story has shifted quickly over the past few weeks, driven largely by a sharp rise in oil prices tied to geopolitical tensions. At first glance, the rise in inflation expectations looks concerning for investment portfolios. Stepping back, however, the message from the market is more reassuring.Higher oil prices are pushing up near-term expected inflation. When energy costs rise, consumers feel it quickly at the pump and in other everyday expenses. This creates a temporary spike in inflation data over the next several months.Markets are signaling that this increase in inflation is likely temporary, with investors expecting inflation to return to more normal levels once the impact of higher oil prices fades.

If investors believed that higher energy prices would lead to sustained inflation, we would see a much stronger reaction in longer-term inflation expectations and treasury bond yields. That has not happened as long-term inflation expectations remain stable even as near-term inflation pressures increase.

Interest Rates

In January, two .25% cuts in short-term interest rates by the Federal Reserve were a foregone conclusion. Given heightened inflation concerns today, the market is pricing in zero cuts for the remainder of the year. Policymakers have made it clear that what matters most is whether inflation expectations stay anchored. So far, the market is signaling confidence that they will.

For long-term interest rates to move meaningfully higher from here, we would need to see signs that inflation is becoming more persistent. That could include rising wage pressures or a loss of confidence in the Fed’s ability to control inflation. We are not seeing that today.

Our view is that the recent rise in long-term interest rates is likely to be nearing its end. As markets continue to look through the current oil-driven inflation spike, rates should stabilize and potentially move lower, supported by long-term inflation expectations that remain under control.

Client Portfolios

In the fourth quarter of last year, we modestly reduced portfolio risk in most client portfolios by trimming allocations to some of the bellwether large-cap technology companies and reinvesting the proceeds in bonds. To date, this shift has proved timely. While we were not bearish on technology stocks, we believed that bond yields offered an opportunity to increase exposure.

With respect to the equity markets, earnings will ultimately dictate their direction. We are heartened that, at this juncture, expectations for 2026 earnings growth remain unwaveringly strong at +15%. Of course, earnings expectations are one of the key variables we constantly monitor, and the direction of future earnings will likely carry the greatest weight in informing our risk appetite in the months ahead.

Disclosure

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.