by Blaine Dickason

Senior Vice President

Portfolio Management and Trading

Rising oil prices, driven by the war in Iran, have reintroduced a familiar dynamic into financial markets. While the sharp increase in gas prices may be the most visible impact for most Americans, additional adjustments across currencies and interest rates have also been notable. The signal from oil has been clear, but the downstream effects remain much less so.

One clear shift so far this year is that oil and the U.S. dollar are now moving in tandem. As the weaker U.S. dollar was a major factor in global stock market returns last year, this represents a notable inflection point. With crude prices pushing above $100 per barrel, the dollar has strengthened alongside it, contradicting last year’s prevailing narrative that the dollar’s global dominance was fading. Instead, recent price action reinforces the opposite conclusion.

This relationship is structural. Oil is priced in U.S. dollars, global trade is financed in dollars, and a large share of global liabilities are dollar-denominated. When energy prices rise, so too does the transactional demand for dollars. What we are seeing is not simply a cyclical move tied to relative growth, but a reflection of the dollar’s entrenched role at the center of the global financial system.

At the same time, higher energy prices are tightening financial conditions. This has been reflected in oil, the dollar and interest rates, which have all risen, while risk assets like stocks have come under pressure. What ultimately matters is not just the direction of oil prices, but how high they rise and how long they remain elevated. A temporary spike is manageable; a sustained period of elevated prices would likely have more meaningful implications for growth, inflation and asset prices.

Interest rates are beginning to reflect this tension. Treasury yields have drifted higher as markets incorporate the possibility that energy-driven inflation may prove more persistent. The degree to which higher oil prices feed into core inflation, and ultimately the Federal Reserve’s monetary policy, remains uncertain, although directionally, they have not been helpful. Bond markets responded to this week’s Middle East developments by pricing in a higher-for-longer expectation for oil prices than previously expected.

This uncertainty was also evident in this week’s FOMC meeting. Fed Chair Jerome Powell signaled a clear pause on earlier expectations of several interest rate cuts later in the year, opting instead to project patience as they assess evolving conditions in both inflation expectations and labor markets. His message was straightforward: policy will remain data-dependent, and the bar for further easing has moved significantly higher.

Source: Bloomberg

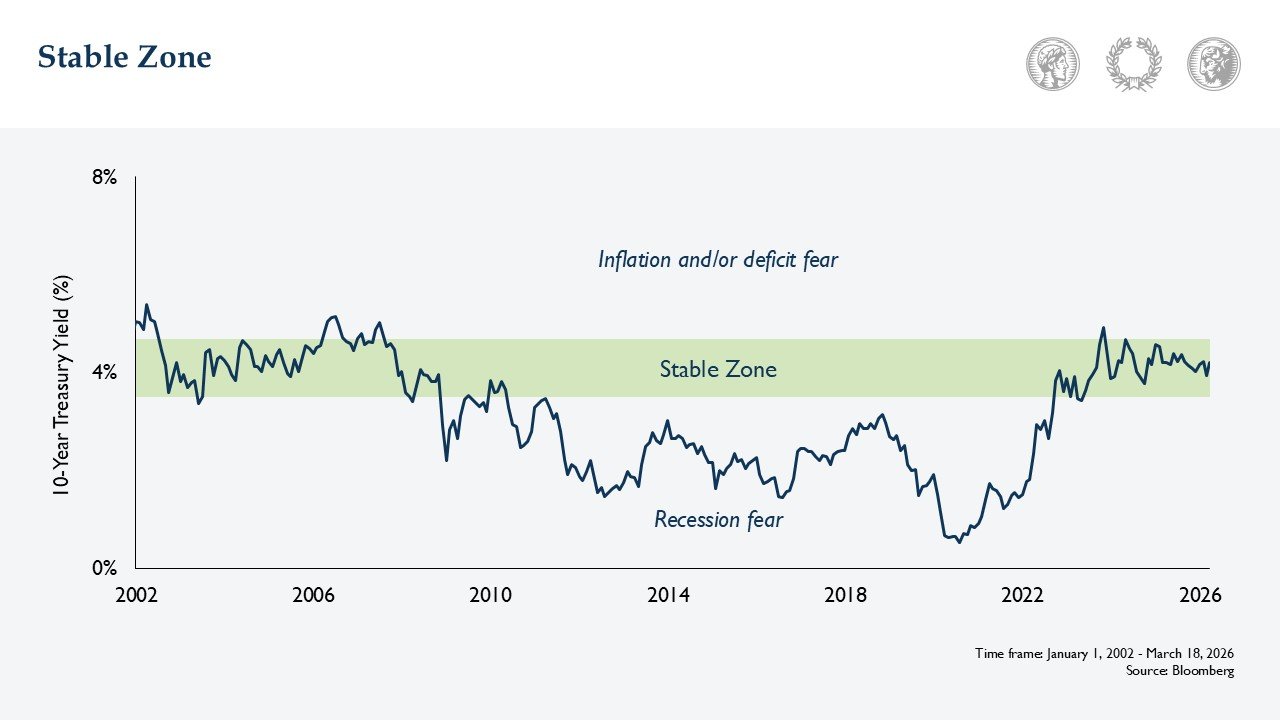

Against this backdrop, the U.S. 10-Year Treasury yield offers a useful lens into how markets are processing these crosscurrents. Since 2002, yields have oscillated within a broad range, but in the current cycle, a “stable zone” between roughly 3.50% and 4.75% has emerged. When yields reside within this range, we presume markets are effectively balancing competing risks. A move above this range would indicate elevated fears of uncontained inflation or financing our government debt, while a level below this range would signal a recession or growth slowdown. The yield on the 10-year Treasury is one of those marquee economic indicators we will continue to watch closely.

Takeaways for the Week:

Gold has traditionally been viewed as a hedge against inflation. This narrative has recently been challenged, as gold’s spot price has declined by 15% since the end of January despite higher inflation expectations driven by rising energy prices. Gold’s recent price action is much more consistent with its ability to act as a hedge against a weakening dollar

Fed Chair Jerome Powell said this week he has “no intention of leaving the Board” of the Federal Reserve until any pending investigation by the DOJ is “well and truly over.” While Powell’s term as Fed Chair officially expires in May, his term as Governor does not officially expire until 2028

Disclosure: The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional Disclosures.