by Reilly Blood, CFP®

Associate Wealth Planner

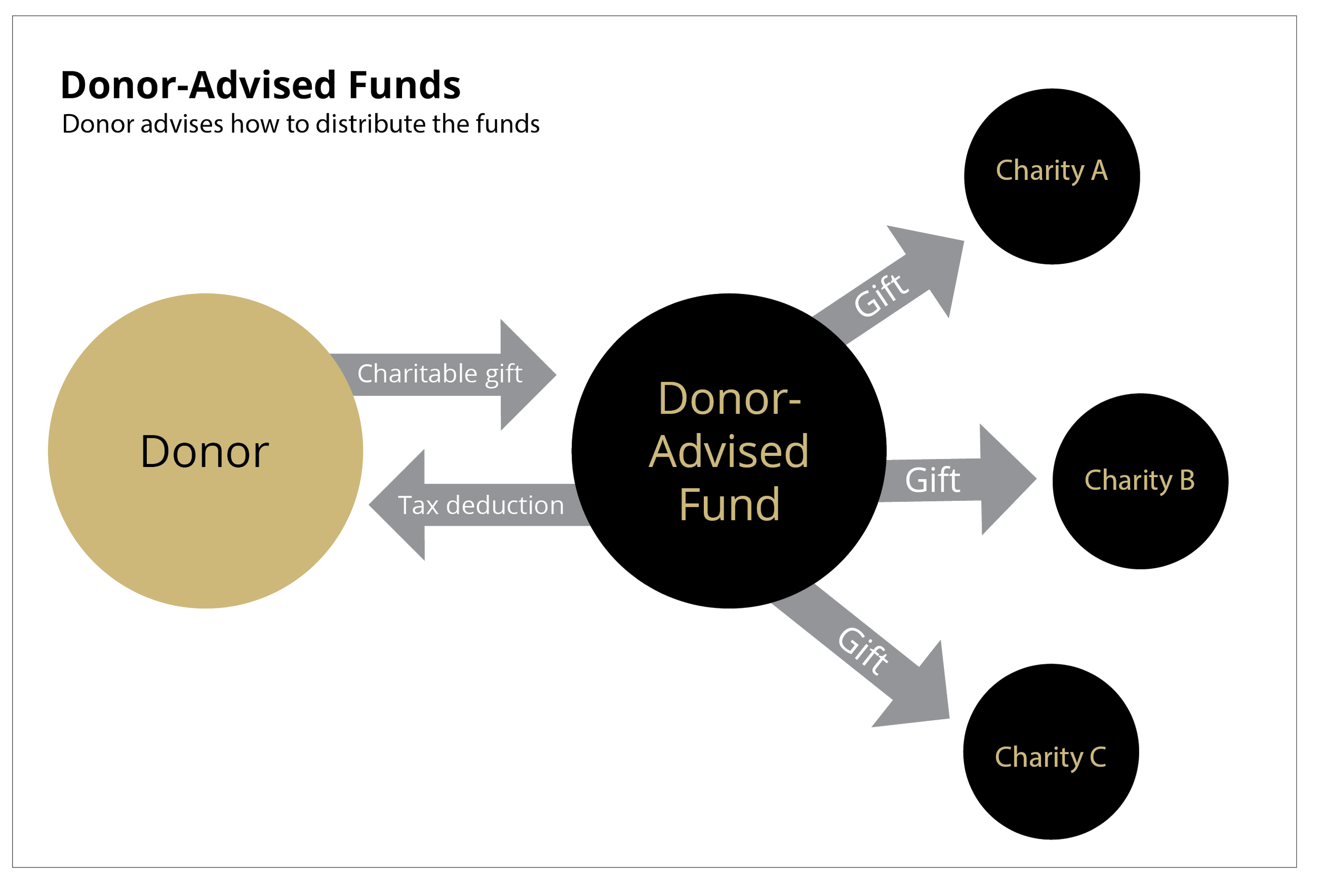

Tax season often sends people searching through old emails, letters and statements to find documents for their tax professionals. Amid this administrative clutter, many look for ways to simplify their charitable reporting. For those who are philanthropically inclined, a donor-advised fund (DAF) can simplify both the giving process and the associated tax paperwork.

What is a Donor-Advised Fund?

Donor-advised funds are charitable accounts that individuals or married couples can establish to streamline the management of their philanthropic goals. Most notably, they are tax-efficient investment vehicles in which funds are permanently set aside for charity. DAFs have become a widely used philanthropic tool because they:

simplify tax reporting and charitable gifting;

create opportunities for tax savings by donating appreciated securities;

provide flexibility in the timing of deductions in a changing tax landscape; and

serve as a low-cost, accessible vehicle for long-term philanthropic planning.

In addition, DAF assets may be invested for future growth before distribution. For Charles Schwab clients, when an account balance exceeds certain thresholds, it can become eligible for investment advisory management, offering the donor greater input over the portfolio investment strategy.

Where Can I Establish a Donor-Advised Fund ?

A DAF must be established through a qualified sponsoring organization, which is a public charity that administers the fund and oversees grants to eligible charitable recipients.

Many large national sponsors, including Charles Schwab’s DAFgiving360, allow donors to initiate and complete the process entirely online with little to no initiation fees. Some have minimum grant requirements; however, many have no minimum balance or additional contribution requirements. These platforms can be especially appealing for donors who value ease of use, broad operational capabilities and integration with existing custodial relationships.

Community foundations may also be a great option for establishing a DAF. In addition to offering the administrative and tax advantages common to many DAF sponsors, community foundations often provide a unique understanding of local needs, nonprofit organizations and regional priorities. For donors who want their charitable giving to have a more targeted local impact, these organizations can serve as a resource for identifying grant opportunities, evaluating community needs and connecting philanthropic intent with on-the-ground initiatives.

Administrative Benefits

A DAF simplifies tax season because contributions and grants are treated differently for tax purposes. When donors contribute to a DAF, that single contribution is what appears on the annual tax receipt—regardless of how many charities ultimately receive grants from the fund. This is especially useful for those who give to multiple organizations throughout the year or who make recurring gifts on an annual basis.

Compared to other philanthropic structures, such as charitable trusts or private foundations, DAFs generally offer:

minimal setup and administrative costs;

no separate tax-return filing; and

fewer required legal documents.

This keeps the focus on charitable intent, rather than administration. In the same vein, donors may also appoint a successor advisor to direct remaining charitable funds after their lifetime, supporting multi-generational philanthropic goals.

Tax Benefits

Donating an asset to a DAF is considered an irrevocable charitable gift. As with gifts to operating charities, the donor(s) no longer personally own the assets once gifted. When long-term appreciated assets are contributed, the donor avoids embedded long-term capital gains that would otherwise be recognized, or taxable, if the securities were sold first and the cash donated second.

DAFs can also enhance tax efficiency through “bunching,” a strategy that consolidates multiple years of anticipated charitable contributions into a single tax year, ideally with the intent of exceeding the standard deduction threshold. Donors may then recommend grants to charities from their DAF in subsequent years, while reverting to claiming the standard deduction in those years

A donor-advised fund can reduce administrative burden at tax time, offer tax benefits and support both near- and long-term charitable legacy planning. Contact your portfolio manager to discuss whether this approach aligns with your broader financial strategy and which assets may be appropriate to contribute.

Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational and informational purposes only and not as a substitute for qualified counsel. We believe the information provided is from reliable sources but should not be assumed accurate or complete. You should consult qualified professionals to understand how this information may, or may not, apply specifically to you.