by Jake Gradwohl

Senior Equity Trader

This week, capital markets’ behavior continued its recent adoption of a “Tortoise and the Hare”-style dynamic, with fast-moving geopolitical headlines driving short-term volatility, while underlying economic trends evolve more gradually. News flow around the conflict in Iran has accelerated to a pace that markets are finding difficult to absorb in real time. In a matter of days, investors have been presented with sharply differing narratives — with some suggesting escalation risks are rising meaningfully, others pointing to potential steps toward conflict resolution, and still others focused on the tangible impact sustained oil price increases could have on consumers’ spending habits. These competing storylines have yet to resolve into a clear macroeconomic conclusion, but have instead contributed to a more reactive market environment.

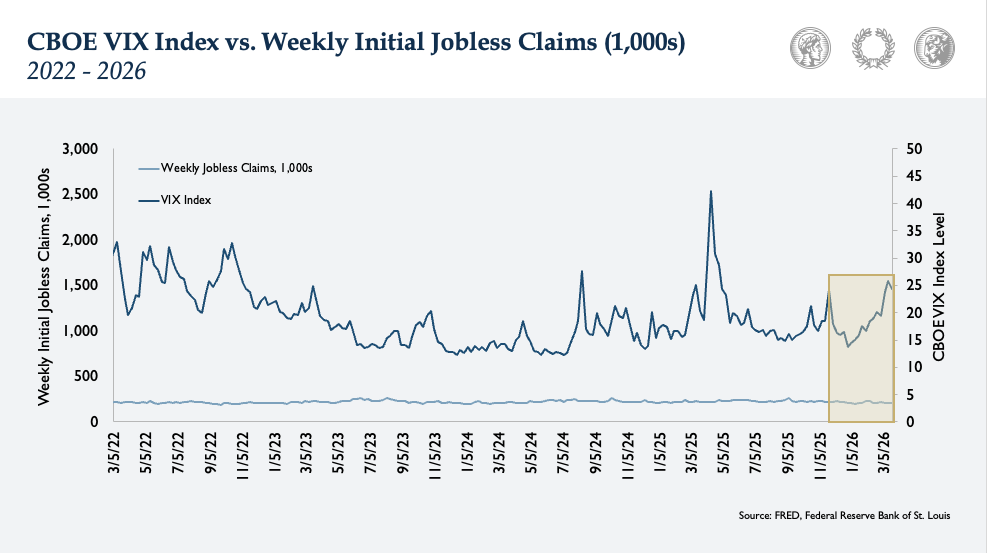

This reactivity is shown in what is commonly referred to as the market’s “fear gauge”, the CBOE Volatility Index (VIX). The VIX measures perceived market volatility based on S&P 500 option prices, which are often interpreted as the cost of market “insurance”. A higher VIX index level indicates a higher cost for these options, representing that investors are willing to pay more for protection against the market volatility they feel exists. Despite beginning the year at a low level, year-to-date, the VIX index has risen to levels not seen since last April’s “liberation day” tariff announcements. While at present it is still below levels associated with more severe periods of market stress, the increase suggests investors are becoming increasingly aware of the persistence of near-term uncertainty. The result is a market environment where sentiment is shifting quickly, even as it remains less clear whether underlying economic conditions are changing at the same pace.

In contrast to the increase in headline-driven market volatility, the labor market has remained notably steady. Weekly initial jobless claims, which measure the number of new unemployment claims filed state-by-state and are especially relevant due to their real-time reporting, have shown only modest movement so far in 2026. More importantly, they also remain close to their historically low levels from this same time last year. In this context, existing job stability matters because labor market conditions are a primary driver of overall economic activity through their influence on households’ income and spending. Low unemployment rates also tend to support consumers’ economic resilience during periods (whether shorter-term or longer-term) of higher inflation and volatility. So far, despite elevated geopolitical uncertainty, unemployment claim stability suggests that volatility hasn’t yet translated into new, material labor market stress.

Taken together, the divergence between intraday volatility and steady labor market data points to a gap between short-term uncertainty and longer-term market expectations. In the near term, the war has introduced a new source of volatility, with rising concern that higher energy prices could push short-term inflation meaningfully above prior forecasts. An estimate published this week by the Organization for Economic Cooperation and Development points to U.S. inflation’s potential to cross roughly 4% this year. This estimate’s upward revision was attributed to the threat of prolonged higher energy prices and the impact such price increases would have on both business costs and consumer demand. It is notably higher than recent inflation readings, including March’s 2.4% year-over-year increase in the headline Consumer Price Index. Interest rate expectations have also shifted alongside that risk; market participants are now expecting no federal funds rate cuts this year and, begrudgingly, are coming to terms with the chance of rates increasing if inflation proves more persistent. However, the longer-term picture remains more stable at the moment. Measures like the five-year forward break-even inflation rate (a market-based gauge of expected inflation over the longer term) have moved relatively little in recent weeks, suggesting that investors still view inflation as ultimately contained. That stability aligns with what we see in other underlying economic drivers: the labor market remains little-changed this year, consumer activity has not materially weakened, and corporate profits have yet to show broad signs of deterioration.

The key distinction at present is that, while conflict in Iran is influencing the path of the next few quarters, it has not yet meaningfully altered the market’s longer-term expectations. However, as our colleague Blaine Dickason discussed last week, a more sustained shock through prolonged and substantial energy cost increases would have the potential to change that thesis. For now, faster-moving headlines continue to drive markets more than slower-moving fundamentals.

Takeaways for the Week

The S&P 500 is on track to post its fifth consecutive weekly decline, and will close below both its 9/30/2025 and 12/31/2025 levels, bringing the index close to correction level down 8% from its high

Weekly initial jobless claims, published on Thursday, increased by only 5,000 to 210,000, which continues to be at the low end of its historic range

Derivatives markets now show 0% chance of a federal funds rate cut in 2026

Disclosure: The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional Disclosures.