by Blaine Dickason

Senior Vice President

Portfolio Management and Trading

Yesterday marked Jerome Powell’s last Thanksgiving as Federal Reserve Chair. While he might have much to be thankful for, this year, as he enters the final months of his chairmanship, a unified Federal Reserve is not one of them. With the next Fed meeting and a possible interest rate cut in less than two weeks, we wanted to highlight the dynamics and implications of several transitions occurring at our country’s central bank.

Transition #1: How many more rate cuts? Are we close to the end of the cutting cycle?

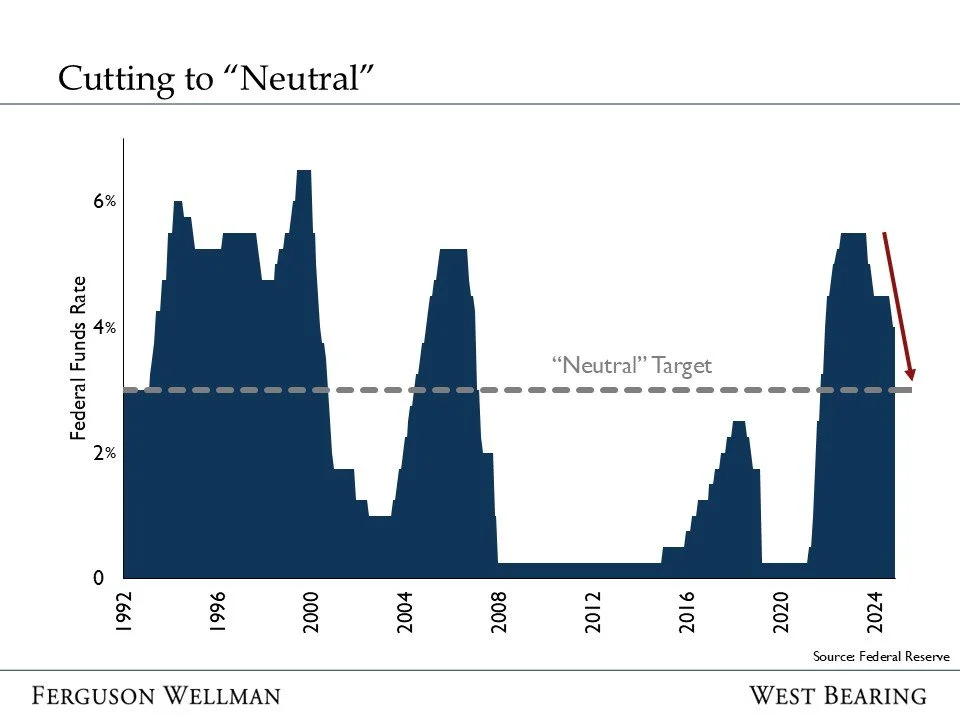

The current expectation is that the Fed will cut its policy interest rate by another 0.25% at its upcoming December 10 meeting; the third rate cut this year. Additionally, this would also mark the sixth cut in the current rate-cutting cycle, which began in September 2024. For the last several years, the Fed’s policy rate has clearly been set in restrictive territory, to combat legacy inflation from the pandemic and, more recently, to offset potential inflationary impulses from increased tariffs. Given strong corporate earnings and continued momentum in the U.S. economy, the Federal Reserve is likely targeting only a return to a neutral interest rate, which, in their view, neither stimulates nor restricts our economy. This “neutral” level cannot be accurately determined; however, based on the Fed’s own projections, it is roughly a 3% Federal Funds rate. Given that framework, and as you can see from the chart below, spanning back to 1992, this implies the Federal Reserve may have only a couple of additional interest rate cuts left in 2026.

Source: Federal Reserve

Transition #2: A new Chair for the Federal Reserve

Jerome Powell was appointed to the Fed’s Board of Governors in 2012 and was elevated to Fed Chair in 2018. After renomination for a second four-year term in 2022, Powell’s term as Chair concludes next May. It is up to President Trump to nominate a successor, who then must be confirmed by Congress. While a short list of likely candidates had already emerged, the White House indicated a preference for Kevin Hassett just in the past week. Mr. Hassett currently serves as the Director of the National Economic Council and is widely viewed as the administration’s top economic advisor. There has typically been a learning curve for both financial markets and a newly appointed Fed chair, as our central bank’s messaging and interest rate policy can have a wide-ranging impact across global markets. Each new Fed Chair has their own communication and leadership style that will need to be accounted for as they steer monetary policy to achieve its dual mandate of maximum employment and price stability for the U.S. economy.

Transition #3: More polarization and competing mandates

This past year has brought increased tension to the Fed’s targeting of both its mandates for maximum employment and price stability (i.e., inflation). Inflation that continues to run above the Fed’s 2% target has emboldened certain members of the Fed’s Board to become vocal “hawks,” advocating for rates to remain in restrictive territory until inflation recedes further. Other members of the Fed Board, including newly appointed Governor Stephen Miran, have strongly advocated for continued cuts to support full employment, as the labor market has shown slowing momentum this year. The net of this more vocal debate is that there appears to be greater polarization among the members of the Fed Board. For an institution that relies on strong communication with financial markets to conduct much of its policy work, a fractious membership is likely to make its job more challenging, which may have implications for heightened market volatility and the likelihood of policy errors.

In conclusion, there are many dimensions to the changes unfolding at the Federal Reserve that are likely to influence how monetary policy is conducted in the near term. While it’s important to appreciate these changes, it’s also important to understand their limitations. For U.S. consumers, the benefit of Fed rate cuts will not necessarily flow straight through to lower the debt burdens of average Americans. Mortgage and car loan rates are also not likely to decline in lockstep with additional cuts. Bringing their policy rate down to their estimation of ‘neutral,’ regardless of who is Fed Chair, will allow other policy priorities by Congress and the administration to take hold without either being stimulated or restricted by the Fed.

Takeaways for the Week

The Fed is expected to deliver another 0.25% interest rate cut at its upcoming meeting on December 10: the third rate cut of 2025

Adobe has estimated that the U.S. consumer is expected to spend a record $11.7 billion online on Black Friday, an increase of 8.3% from 2024 (Business Insider)