by Jason Norris, CFA

Director

Equity Research and Portfolio Management

“In the short term, the market is a voting machine. In the long term, it is a weighing machine.” - Warren Buffett

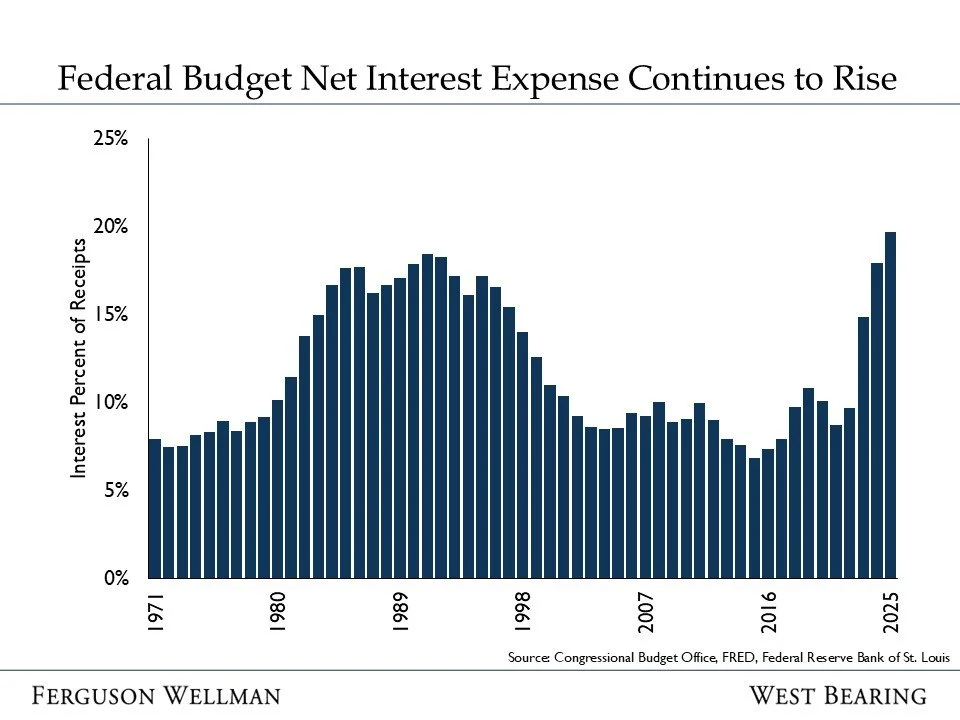

This week, the Congressional Budget Office released its estimate of the federal government’s fiscal year 2025 budget deficit. Nine months ago, there were high expectations that policymakers would move to reduce the deficit spending we’ve seen over the last 25 years. In January, we discussed this in our Investment Outlook, stating that we would take the “under” with respect to spending cuts. While we saw tax revenues grow faster than expenditure, 6% versus 4% respectively, the net interest expense for the federal government rose to $1.03 trillion. This cost now comprises 20% of total federal revenue. The chart below shows the progression of interest costs as a percentage of revenues at all-time highs.

Source: Congressional Budget Office, FRED, Federal Reserve Bank of St. Louis

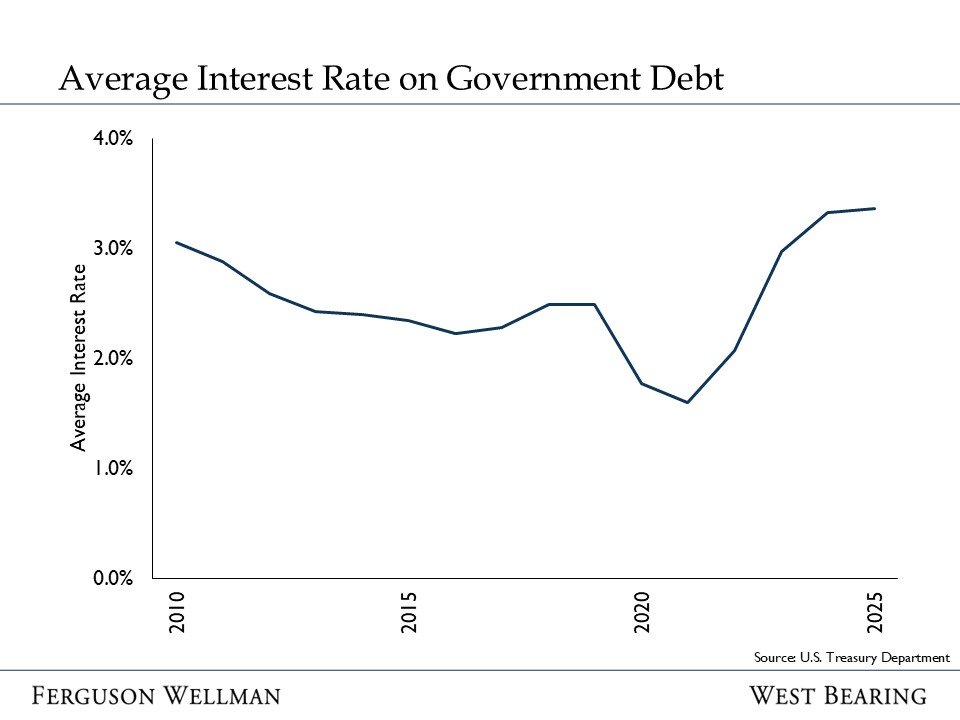

The increase was due to two factors. First, spending was close to $2.0 trillion more than what was being collected. Second, the interest rate on the national debt continues to increase. In fiscal 2025, the average interest rate on government debt was 3.4%, comparable to 2024, but nearly 1% higher than the average rate over the last 15 years.

Source: U.S. Treasury Department

With our expectations that short-term interest rates will fall modestly and long-term rates will stay in their current range, we don’t expect a major change in financing costs in the next year or so. The key question is, “When will this come home to roost?” — unfortunately, we have yet to see any desire or action from either political party to lower the deficit. Thus, over the next few years, we could see a move to higher taxes and lower spending, which would be a headwind to growth. However, for now, we are in a stimulative state.

This week, investors celebrated the third anniversary of the bull market. The S&P 500 hit a low in October 2022, and since then, the total return has roughly doubled. Markets also celebrated the six months since the April “tariff tantrum” bottom with stocks rallying 35% over that period. We highlight these instances to remind clients of two key points: first, markets are volatile, and second, time horizon is crucial. Knowing your investment time horizon and having the appropriate asset allocation for your overall risk/return objectives is essential. Investing in volatile times can increase anxiety; however, focusing on your long-term objectives and understanding the current situation and historical context is important.

Takeaways for the Week

Stocks sold off Friday, falling 2% for the week as Chinese tariff threats boiled over. As we’ve seen in the past, tariff rhetoric elevates stock market volatility

Bonds rallied as a result of these concerns, bringing the 10-Year Government bond yield down to 4.05%. We’ve stated in the past that yields below 4% aren’t too alarming, but closer to 3.5% would be a concern