by Jason Norris, CFA

Executive Vice President of Research

Stocks posted a 0.5 percent return this week as investors became more confident in economic and fiscal policies. The Dow Jones Industrial Average passed 21,000 for the first time and equities posted their first 1 percent day in over four months. This rally also resulted in a sell-off in bonds. The yield on the 10-year Treasury rose 14 bps to 2.51 percent.

The Good News First

Source: CNBC

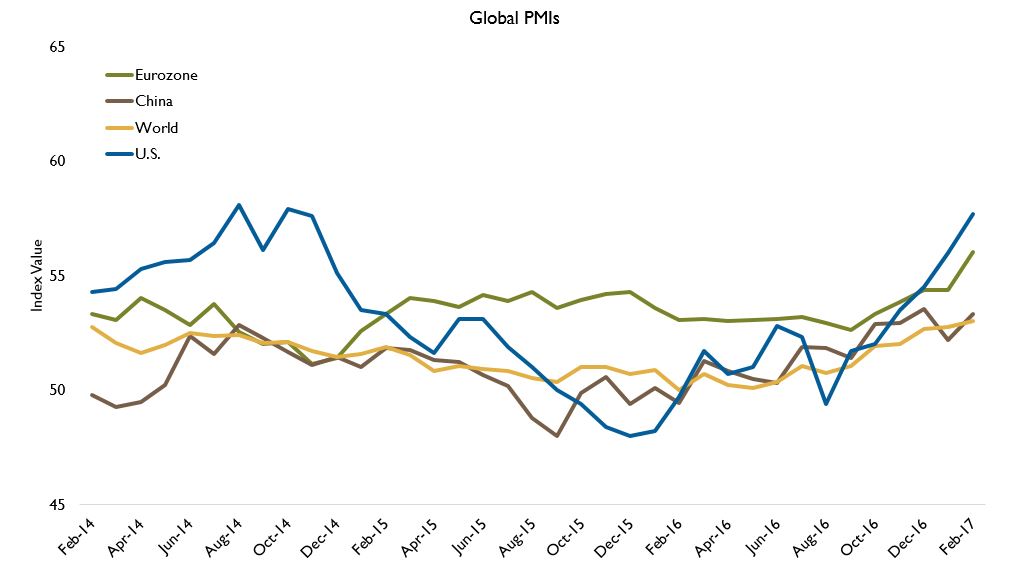

There has been a lot of media attributing this recent rally to President Trump. However, we believe this matter to be more complex. While some of his proposals are more business-friendly, we believe that the timing of them will be longer in duration than the market expects and this rally is warranted due to the strength of the U.S. economy. On Thursday, weekly jobless claims hit a 40-year low. On Wednesday, global manufacturing Purchasing Managers' Indices (PMIs) continued to show strength. The chart below shows the strong trends in PMIs which are leading indicators for GDP growth.

Source: FactSet

While we believe that there has been a rebound in so-called “animal spirits,” the turn in the economy started back in late summer. This is important because if fiscal policy changes take too long or aren’t effective, the economy will still be on sound footing. This is the most important factor for a reacceleration in earnings growth.

With equities rising 7 percent so far this year, surpassing most strategist’s targets for 2017, the question is, “Where do we go from here?” We currently aren’t reducing equity exposure and would become more bullish if we continue to see a reacceleration earnings growth in 2017. However, history is on the side of the equity market for 2017. Since 1950, when stocks were positive for the first two months of the year, equities will continue to grind higher as seen in the chart below.

Source: Strategas

What makes this more compelling, is that even with the 11.5 percent return, stocks are at least positive 92 percent of the time.

Retail Woes

It was a tough week for some major retailers. Both Target and Costco reported disappointing earnings. As more consumers shift to online shopping, the retail space will have to adjust. However, it has been shown that that is easier said than done. And while we believe there are opportunities, investors must continue to be very selective.

Our Takeaways for the Week:

The U.S. economy continues to improve which is helping drive equity prices

Have we come too far, too fast? We will know if first quarter earnings can justify valuations