by Shawn Narancich, CFAExecutive Vice President of Research

by Shawn Narancich, CFAExecutive Vice President of Research

Working for a Living

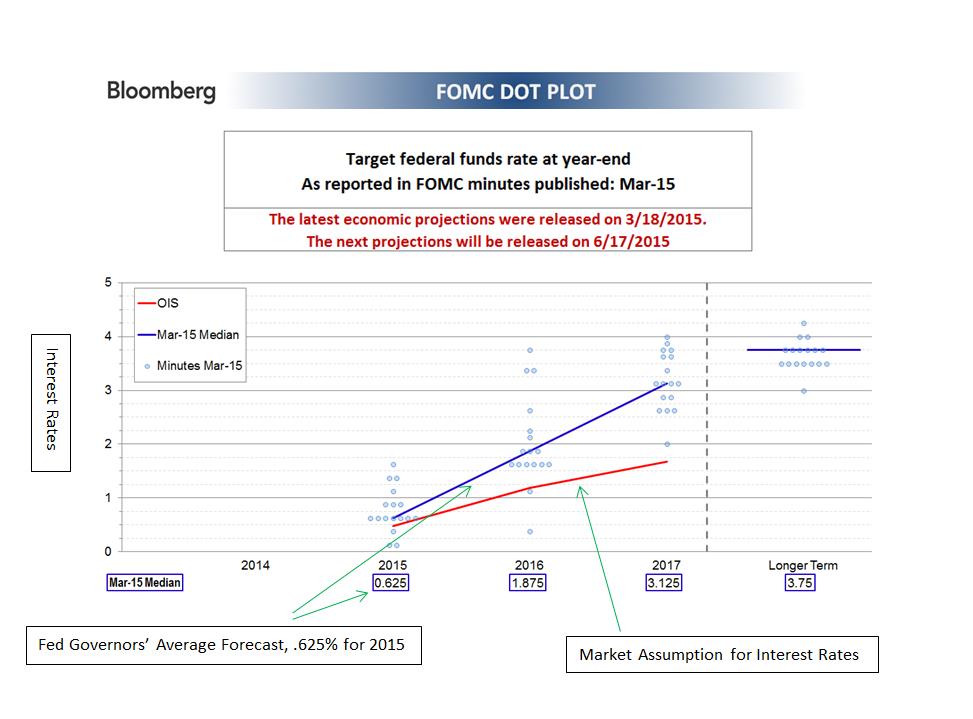

Investors unnerved by disappointing economic data of late breathed a sigh of relief with the April jobs report, which showed that nonfarm payrolls rebounded to a monthly rate of 223,000 last month. Unemployment dropped again and now stands at 5.4 percent, a rate not too far from the Fed’s definition of the full employment rate of unemployment (somewhere just north of 5 percent.) A “goldilocks” report of sorts that’s neither too hot nor too cold, the April payroll release supports the notion that the Yellen & Co. will likely begin the rate tightening process this fall. As policymakers and investors debate how tight labor markets actually are against a backdrop where the labor force participation rate hovers near its lowest level since the late 1970s, we are increasingly attuned to reported wage rates and the broader employment cost index (ECI). While wage gains remain muted at 2.2 percent in April, the ECI of 2.6 percent released last week demonstrated a notable uptick. When juxtaposed against anecdotal evidence of wage gains at fast food restaurants and retailers, our best guess is that the worm has turned with regard to employment costs this cycle. Because labor accounts for the predominant cost of doing business, the near-zero inflation rates we’ve seen of late appear likely to begin rising. When combined with the recent rebound in oil prices, headline inflation probably rises closer to the Fed’s 2 percent target by year-end.

Spring Forward

In contrast to the encouraging labor report, investors were greeted by a report showing that productivity of the U.S. labor force declined for the second consecutive quarter. While somewhat obscure, the statistic shines a light on the U.S. economy’s weak start to the year. By marrying employment and output statistics, the report tells us that the U.S. economy produced less per each hour worked in the first quarter. The reason productivity is such an important statistic is because when it’s combined with employment costs, it generates what we call unit labor costs. As alluded to above, sustained increases in the cost of labor are a key signpost for inflation, particularly when they translate into rising costs of production on a per unit basis. Just as importantly, unit labor costs determine how profitable companies are and the overall standard of living enjoyed by workers. Another tough winter combined with disruptions from the west coast ports strike put a damper on the U.S. economy in the first quarter, but we believe that an improving labor market, rising disposable incomes, and higher capital spending will engender a rebound of sorts in the second quarter. Commensurately, we would expect productivity to return to positive territory.

Exceeding Expectations

First quarter earnings season is just about finished and, once again, U.S. companies have done a remarkable job of under promising and over delivering. Compared with expectations of a low single-digit decline in first quarter profits, corporate America is instead delivering earnings that should end up being marginally above levels of a year ago. In particular, while dramatically lower oil prices caused red ink to flow on the income statements of many energy companies, the damage was ameliorated by better downstream refining and marketing results and the quick pace with which oil and gas producers have right-sized their cost structure.

Our Takeaways from the Week

- A solid April employment report bodes well for better economic times ahead

- Another encouraging earnings season is just about finished

{kind=link}