Please click here to find our Market Letter First Quarter 2015. We hope you find our economic insights interesting and informative.

2015 Q1 Market Letter

Volatility aside, 2015 is playing out much the way we anticipated. Europe’s central bank has graduated from talking about quantitative easing (QE) to actually delivering on it, and with $1.1 trillion of bond purchases planned for the next 18 months, markets

2015 Investment Outlook Video: Riding the Global Liquidity Peloton

We are pleased to present our 2015 Investment Outlook video titled, "Riding the Global Liquidity Peloton." Ralph Cole, CFA, executive vice president of research and Investment Policy Committee member, discusses what we believe will occur in the markets in 2015.

To view this 12-minute video, please click here or on the image below.

Intro slide

Fourth Quarter 2014 Investment Outlook Video: Not Too Hot, Not Too Cold

We are pleased to present our Investment Outlook: Fourth Quarter 2014 video titled, "Not Too Hot, Not Too Cold." This quarter, Chief Investment Officer George Hosfield, CFA, addresses the factors contributing to recent market volatility and what that means for our outlook going forward.

To view our Investment Outlook video, please click here or on the image below.

Q4_Strategy_IntroSlide

Investment Outlook Video: Third Quarter 2014

We are pleased to present our Investment Outlook: Third Quarter 2014 video titled, "Back on Track." This quarter, Chief Investment Officer George Hosfield, CFA, discusses how despite starting the year with a winter-induced swoon, the equity markets have nearly realized the “average annual return” that we predicted in January for the entire year. That said, we believe that an improving labor market, a strengthening economy, rising earnings, low interest rates and reasonable multiples provide a backdrop for further equity gains.

To view our Investment Outlook video, please click here or click on the image below.

jpeg of Q3 2014 Outlook video for email hyperlink

2014 Q2 Market Letter

Please click here to find our Market Letter Second Quarter 2014. We hope you find our economic insights interesting and informative.

Investment Outlook Video: Second Quarter 2014

We are pleased to present our Investment Outlook: Second Quarter 2014 video titled, "Spring Thaw". This quarter, Chief Investment Officer George Hosfield, CFA, discusses how the weather impacted the economy and what we believe that means for the continued recovery.

To view our Investment Outlook video, please click here or click on the image below.

jpeg of Q2 2014 video

Investment Outlook Video: First Quarter 2014

We are pleased to present our Investment Outlook: First Quarter 2014 video titled, “Removing the Training Wheels.” This quarter, Chief Investment Officer George Hosfield, CFA, discusses how the Fed will approach tapering of quantitative easing and what we believe will occur in the economy, particularly in regards to the unemployment rate, interest rates and stock market return expectations.

To view our Investment Outlook, please click here or on the image below.

jpeg of Q1 2014 Outlook video for email hyperlink

Investment Strategy Update – 6/17/13

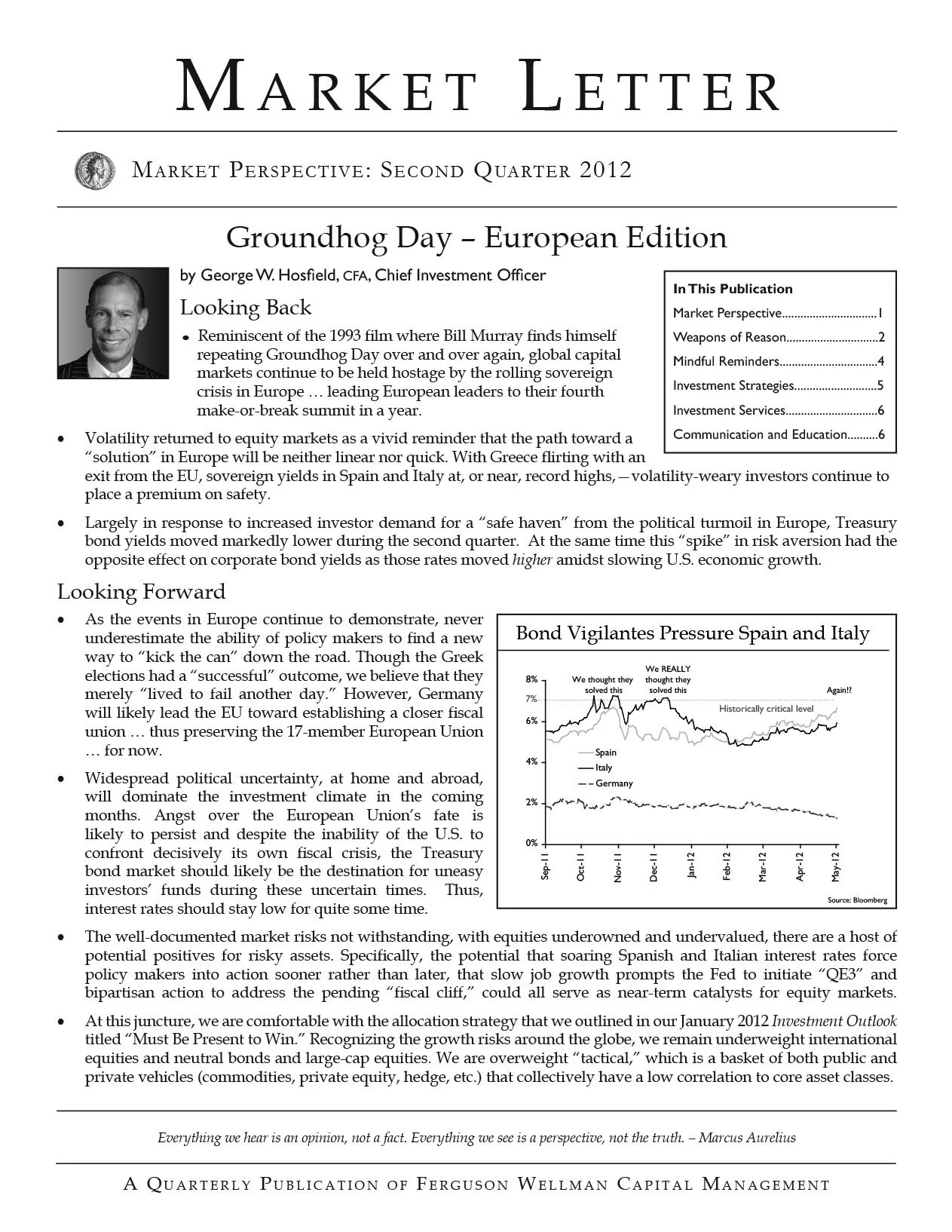

Beginning of the Bond Bear Market?

Interest rates have been moving upward. After peaking in mid-March at 2.06 percent, the yield of the 10-year U.S. Treasury dropped to 1.63 percent in early May. Since then, the yield has spiked to over 2.20 percent. Much of the rise can be attributed to Federal Reserve governors opining on whether the Fed should begin reducing its monthly purchases of $85 billion in securities at some point later this year.

This potential change in strategy has been referred to as “tapering” in the financial media. Rather than actively draining reserves from the system or increasing short-term interest rates, the Federal Reserve would simply purchase fewer securities than in the past. This would be a very minor change in strategy; however, the bond market has interpreted it as a turning point in the interest rate cycle and some commentators are calling it “the beginning of the bond bear market.”

Given the recent upward move in rates and the media chatter on a bond bear market, we thought it would be timely to review our fixed income outlook and strategy.

Though we expect some second half economic acceleration, our outlook is for continued below-trend GDP growth (2 to 3 percent) for this year and next. We believe that significant fiscal stimulus cannot happen with our budget constraints, and with interest rates this low, monetary policy is “pushing on a string.” Coupled with persistent slack in the labor market, this translates to slow growth which translates into slow employment growth and wage gains, as well as tame inflation. These are not the makings of a bond market rout. Nonetheless, we believe the economy will find firm enough footing late this year or early next for the Fed to "taper" its $85 billion-per-month purchases of securities. "Taper" refers to reducing the amount of fixed income securities the Fed purchases each month. Thus tapering still adds money to the financial system, just at a slower rate. The recent rise in interest rates is the bond market discounting this occurrence. As exhibited in the accompanying graph, the yield of the 10-year Treasury has now moved into the lower half of our 2013 forecasted trading range of 2.0 to 2.5 percent.

The bond market is behaving largely as we have expected: a measured rise in rates. With our mildly bearish outlook for bonds, we still believe that being modestly short of our duration benchmarks is appropriate. That said, in a diversified portfolio for a long-term investor, there should always be some allocation to long-term bonds for reasons of diversification, yield, and a hedge against uncertainty. Therefore, even if we become more bearish on bonds, we expect portfolios to still contain a small allocation to long-term bonds.

In balanced portfolios, we are significantly underweight to bonds. Naturally, we are continually monitoring the macroeconomic landscape to determine if a change in strategy is warranted. While there is some room to express greater bearishness on bonds, we feel the current short duration and underweight allocation are currently appropriate in this economic and market environment.

Best regards, Fixed Income Team Marc Fovinci, CFA Brad Houle, CFA Deidra Krys-Rusoff Joe Brooks

How the Compromise Affects Taxpayers … and the Economy**

With a fiscal cliff compromise just signed by President Obama, investors breathed a sigh of relief yesterday, bidding up stocks over 2 percent and sending bond yields up. The bill, H.R. 8: American Taxpayer Relief Act of 2012, covered many provisions of the tax code, but the major changes that high-income Americans will see in 2013 compared to 2012 include:

- A top income tax rate of 39.6 percent for individuals above $400,000 and for those with joint taxable income over $450,000

- A permanent Alternative Minimum (AMT) patch. The exemption amounts are now $50,600 for individuals and $78,750 for households, and indexes the exemption and phaseout amounts thereafter

- A top capital gains tax and dividend tax of 20 percent for income above the same amounts listed above

- Phaseout of exemptions and deductions for adjusted gross income above $250,000 for individuals and for those with joint taxable income over $300,000

- Expiration of the payroll tax cut, increasing the payroll tax rate by 2 percent on the first $113,700 of income

- The $5 million estate, gift and generation-skipping transfer tax for individuals and $10 million for households is now indexed to inflation, but sets the top estate tax rate at 40 percent

These tax increases, combined with the sequestration spending cuts to take effect on March 1, will result in a roughly 1.5 percent hit to GDP in 2013. Despite this austerity, the federal budget will still run in the red, increasing the U.S. national debt level. While the cliff crisis has been temporarily averted, politicians will deal with the sequestration budget cuts and debt ceiling limit over the next two months. The drama is definitely not over.

Even though GDP growth will be below long-run trend, the austerity measures may be coming at a relatively good time. With the housing market turning as well as oil and gas spending ramping up, economic growth should still be able to post 1 to 2 percent in gains. Corporate profits should therefore remain healthy, potentially resulting in gains for equities. Besides the political drama, our main concern in 2013 will be consumer spending. With the expiration of the payroll tax and the increase in taxes on higher incomes, the federal government is taking money out of consumers' pockets. Against this backdrop, the Federal Reserve continues to keep the financial system awash in cash, which should continue to provide some monetary stimulus in the face of fiscal austerity.

While interest rates are trading at the higher end of their recent trading range, we still believe rates will remain lower, longer due to slow economic growth and continued Fed stimulus. We will continue to maintain our bond positions while Washington still grapples with the remaining “cliff” issues on the table.

**Any tax information in this communication is not intended or written by Ferguson Wellman Capital Management to be used, and cannot be used, by a client or any other person or entity for the purpose of (i) avoiding penalties that may be imposed on any taxpayer or (ii) promoting, marketing or recommending to another party any matters addressed herein. And advice in this communication is limited to the conclusions specifically set forth herein and is based on the completeness and accuracy of the stated facts, assumptions and/or representations included. In rendering our advice, we may consider tax authorities that are subject to change, retroactively and/or prospectively, and any such changes could affect the validity of our advice. We will not update our advice for subsequent changes or modifications to the law and regulations, or to the judicial and administrative interpretations thereof.**

The information provided herein is for educational purposes only and should not be construed as investment advice or as an offer or solicitation. Not all securities are suitable investments for all investors; therefore, Ferguson Wellman Capital Management will not necessarily implement any particular strategies discussed herein for all clients. We recommend that you discuss questions regarding your individual portfolio and investment strategies with your portfolio manager.

2012 Q2 Market Letter

2012 Q3 Market Letter

2012 Q1 Market Letter

First Quarter 2012 – Outlook for 2012 by George Hosfield, Fixed Income by Marc Fovinci, Municipal Bonds by Deidra Krys-Rusoff, REITs by Ralph Cole, Dividend Value by Jason Norris, Strategic Opportunities by Dean Dordevic, International by Ralph Cole, Alternative Investments by Dean Dordevic.

Outlook 2012

Last year was one of the most volatile periods in the history of the U.S. stock market. The Japanese earthquake and tsunami, a festering European debt crisis and dysfunctional U.S. politics weighed on consumer, business and investor sentiment in 2011—creating economic and market headwinds. Having endured a decade of boom and bust cycles in technology, real estate and commodities—U.S. investors are fatigued by a roller coaster stock market that has made little forward progress.

2011 Q3 Market Letter

Third Quarter 2011 – Looking Back and Forward by George Hosfield, “China Derailed” by Dean Dordevic, Mindful Reminders by Mary Faulkner, Investment Strategies: Large Cap Div Val by Jason Norris, It’s Never Too Early to Start Tax Planning by Mark Kralj and New Look and Functionality for Our Website by Natalie Miller and Shawn Swagerty.

2011 Q2 Market Letter

Outlook 2011

2010 drew to a close with fears of a double-dip recession abating and economic data revealing that the global expansion was intact and gaining momentum. After a mid-year slowdown, the preponderance of economic indicators now point toward a modest reacceleration in domestic growth. For all that was written about the “new normal,” last year looked surprisingly like the “old normal.” Looking forward, the extension of Bush-era tax cuts suggests that the pace of activity will likely accelerate in the first half of 2011 and a second round of quantitative easing (“QE2”) renders a “double dip” highly unlikely. In our view the cyclical equity bull market is not yet over.

2011 Q1 Market Letter

First Quarter 2011 – Looking Back and Looking Forward by George Hosfield, “Rough Rice II: Fat Tails Wag the Dog” by Dean Dordevic, Mindful Reminders by Mary Faulkner, Municipal Bonds by Deidra Krys-Rusoff, Client Balance Sheet by Nathan Ayotte, Delivering our Investment Outlook: Events and Videos by Natalie Miller.

2010 Q3 Market Letter

Third Quarter 2010 – Market Outlook by George Hosfield, “QE2 and the Square Root Redux” by Dean Dordevic, Year-End Tax Changes, Longevity and Continuity piece on Luz Garcia, Kathi Kimes and Kerrie Young.