by Ralph Cole, CFA

Executive Vice President of Research

by Ralph Cole, CFA

Executive Vice President of Research

Although this time of year is often described as the summer doldrums, that certainly was not the case this week. Earnings, the Fed and economic data dominated the tape … and made for interesting market activity.

All Along the Watchtower

Fed-watching during a time of taper is an essential part of managing money these days. The Federal Open Market Committee (FOMC) announced on Wednesday that they would continue to taper their purchases of Treasuries and mortgage-backed securities by an additional $5 billion each this month. The Fed continues on pace to stop all security purchases by October. While they made mention that there is still slack in the labor market, the Fed must be comforted by the consistency of job growth in 2014. The U.S. has added an average of 230,000 jobs per month this year versus 194,000 per month in 2013. Commentary after their two-day meeting continues to signal that they are on pace to begin raising rates in the middle of 2015.

Too Hot?

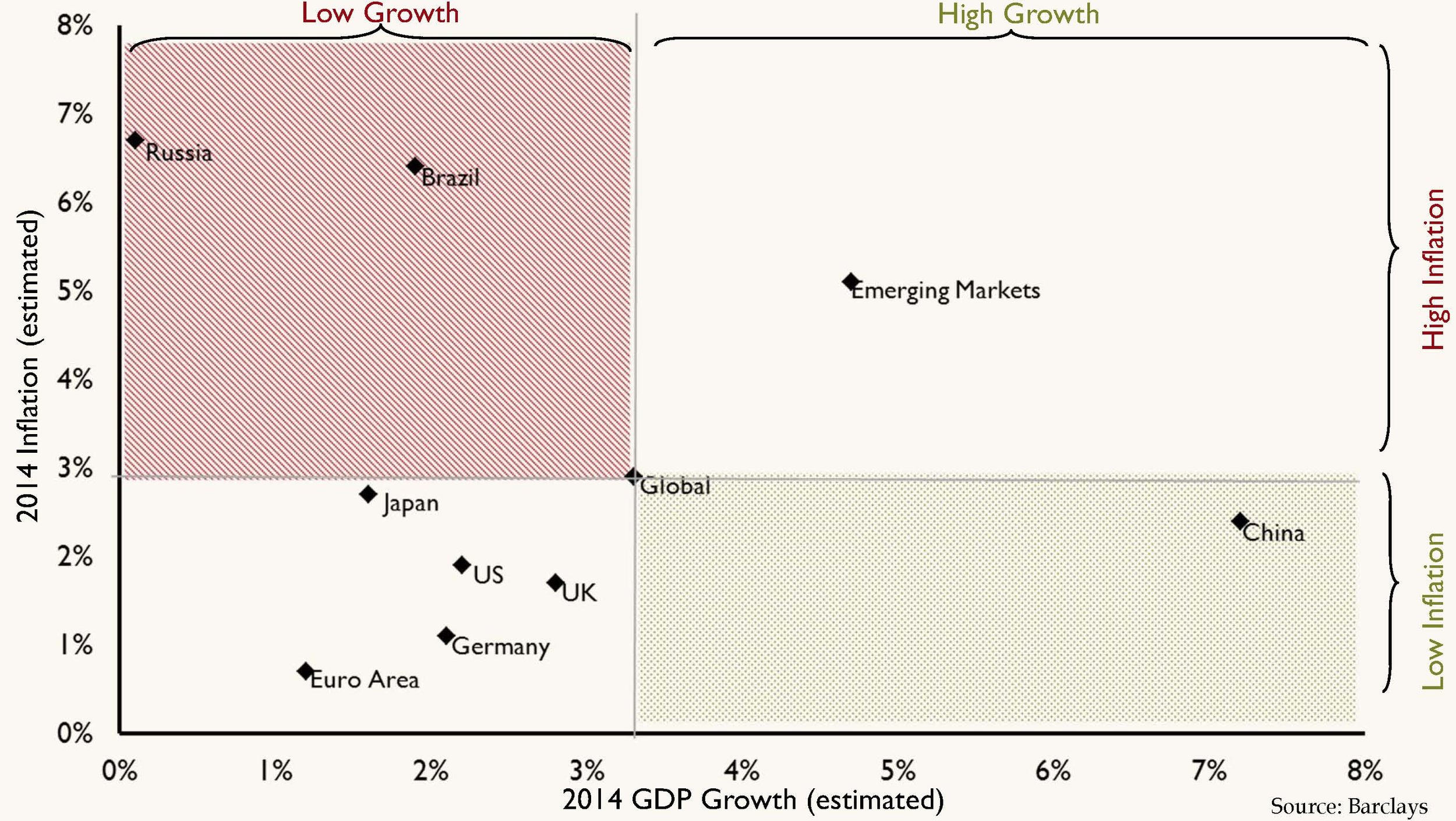

The Bureau of Economic Analysis reported that U.S. GDP grew 4 percent during the second quarter. This robust growth and some of the comments by the Fed may have spooked investors this week into thinking that the Fed will raise rates sooner than expected. We believe this was more of an excuse for a sell off rather than a good reason for selling stocks. There will be volatility in the stock market as we move into next year and the Fed communicates their outlook. In the end, we believe that they will be raising rates for the right reasons … the economy is getting better and extraordinary stimulus is no longer needed.

Upside Down

Earnings season is always one of the more volatile times of the quarter. While earnings have come in very strong (7.7 percent growth up to this point), seemingly minor misses are punished unmercilessly. The healthcare sector has provided the biggest positive surprise for the quarter. Thus far, healthcare companies have reported 14.8 percent growth. On the other end of the spectrum, consumer discretionary companies have only reported 2.9 percent earnings growth.

Our Takeaways for the Week

- Focus on the Fed will continue to cause volatility in the market in the coming months. We believe it is more important to focus on the overall trajectory of the economy to determine direction of the stock market

- Companies continue to grow earnings at an impressive rate despite sub-par global growth