by Peter Jones, CFA

Executive Vice President

Equity Research and Portfolio Management

The second quarter officially ended this week. The main story of the quarter was the powerful snapback in markets after the correction at the onset of the Iran war. Geopolitical fears temporarily tested nerves, but rather than spiraling into a prolonged drawdown, equities quickly digested the anxieties and staged a ferocious recovery, with the S&P 500 returning 15.2%.

The primary engine behind the market’s recovery was the global semiconductor complex. Driven by an insatiable demand for computing power, the silicon giants that form the bedrock of the modern digital economy posted historic, market-leading gains. Specifically, the “SOXX”, an ETF tracking global semiconductor companies, returned a staggering 95% return in the second quarter, driving more than half of the gain in global equity markets.

As we enter the second half of the year, our forward outlook remains constructive. We are using the following takeaways as our primary framework:

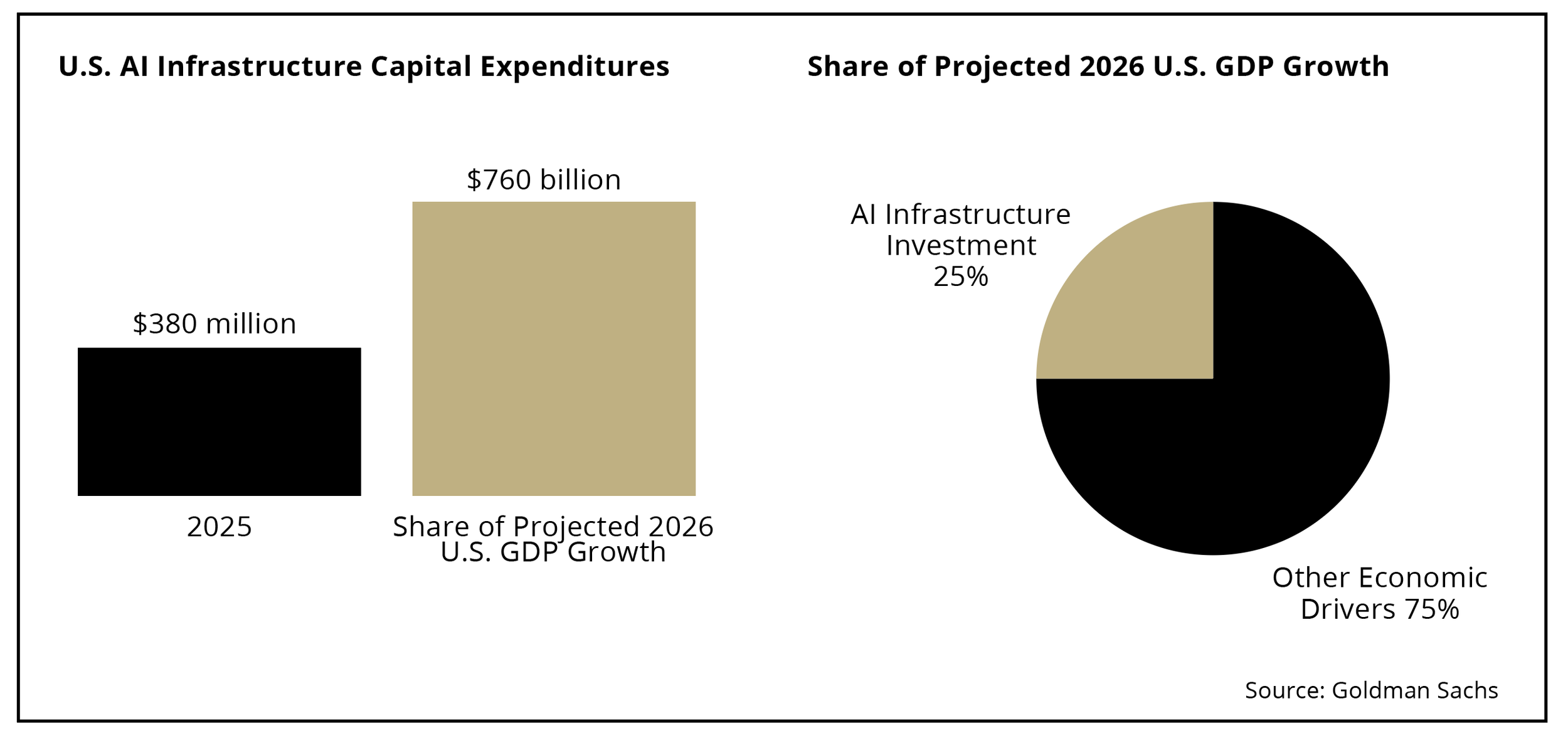

1. Earnings are surging, largely due to AI infrastructure investment. This rally is backed by the fundamentals. Corporate profits are accelerating rapidly, driven by monumental capital expenditures. As the chart below illustrates, U.S. AI capital expenditures are scaling at breathtaking speed, projected to double from $380 billion in 2025 to $760 billion. Crucially, while this AI infrastructure investment currently represents just 1.5% of total U.S. GDP, it is expected to drive 25% of all projected 2026 U.S. GDP growth.

2. S&P 500 returns are up 10% this year, but valuations are actually cheaper than on January 1. It may sound counterintuitive given the recent rally, but the market is fundamentally cheaper today than it was at the start of the year. Because corporate profit generation has expanded faster than stock price gains, price-to-earnings multiples have actually compressed. Simply put, investors are paying less per dollar of earnings today than they did six months ago.

3. Inflation remaining above 4% is high on our list of worries; however, the AI investment cycle breaking is low on our list of worries. Risk management requires prioritizing threats. Currently, sticky inflation dictates the cost of capital and complicates the Federal Reserve’s path, keeping it high on our radar. Conversely, the idea of the AI infrastructure build-out suddenly halting is a less immediate threat to the balance of 2026. The massive capital commitments from major tech firms show no signs of slowing in this “AI arms race.”

American Ledger: A 250-Year Financial Perspective

With our country reflecting this summer on the Spirit of '76, our team recounts how 2026 economic themes have evolved from our founding days.

As we look over the horizon, 2026 will not just be a year of projected AI-driven economic growth—it will also mark the USA's 250th anniversary. While seemingly on the back burner compared to 2025, tariff policy remains a persistent media topic and concern for investors. While tariffs are elevated compared to any other period in the modern era, a look back to our nation's founding illustrates that tariffs were once much higher, as they were the primary source of government revenue.

When the Constitution took effect in 1789, the federal government faced an immediate challenge: establishing a stable financial foundation for a young nation burdened by Revolutionary War debt. One of the first major acts passed by Congress was the Tariff Act of 1789, followed by legislation creating a national customs system to collect duties at America's ports. As the nation's first Secretary of the Treasury, Alexander Hamilton was responsible for the repayment of debts related to the Revolutionary War. To do so, he built the federal government's revenue system largely around customs duties, while also promoting policies designed to strengthen public credit and encourage domestic economic development.

The average tariff rates saw a dramatic increase from 20% to 55% between 1790 and 1860, before declining again. This period is characterized by a protective movement that began to take shape after the War of 1812, as the U.S. sought to bolster its manufacturing sector against foreign competition.

Today's tariffs serve a different purpose. Customs duties now account for only a small share of federal revenue, but trade policy has once again become an important economic tool. Policymakers increasingly use tariffs to encourage domestic investment, strengthen critical supply chains and address national security concerns in industries ranging from semiconductors to advanced manufacturing. Although economists continue to debate their long-term costs and benefits, tariffs have reemerged as a central feature of discussions surrounding globalization and industrial policy.

Two hundred and fifty years after America's founding, the role of tariffs has evolved alongside the American economy itself. What began primarily as a practical way to finance a new government has become a strategic policy instrument in a far more complex global economy. Yet one lesson has endured through the centuries: economic policy is often shaped not only by the challenges of the moment, but by the long-term objective of building a more resilient and prosperous nation.

Takeaways for the Week

Markets surged in the second quarter, shrugging off geopolitical risk

Earnings growth is outpacing stock price appreciation

We view inflation as a greater risk than the end of the AI investment cycle

Disclosures

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.