by Brad Houle, CFA

Principal

Head of Fixed Income

Portfolio Management

Bond markets have sold off sharply in recent weeks as investors react to rising oil prices, renewed inflation concerns and growing global fiscal pressures. The U.S. 30-year Treasury yield recently moved above 5.1%, reaching levels not seen in more than two decades and reigniting concerns about the impact of higher rates on both stocks and bonds.

The primary catalyst has been the surge in energy prices following escalating tensions in the Middle East and disruptions surrounding the Strait of Hormuz. Oil markets moved quickly, and inflation expectations followed.

Markets responded by rapidly repricing Federal Reserve expectations. Earlier assumptions for two .25% rate cuts in 2026 have changed to a 100% chance of a rate increase in 2026. In addition, Treasury yields moved sharply higher across the curve.

Still, we believe it is important to distinguish between a temporary energy-driven inflation shock and a structural inflation problem. The U.S. headline inflation reading was 3.8% for the month of April this year, up considerably from the 2.74% inflation reading for December of 2025.

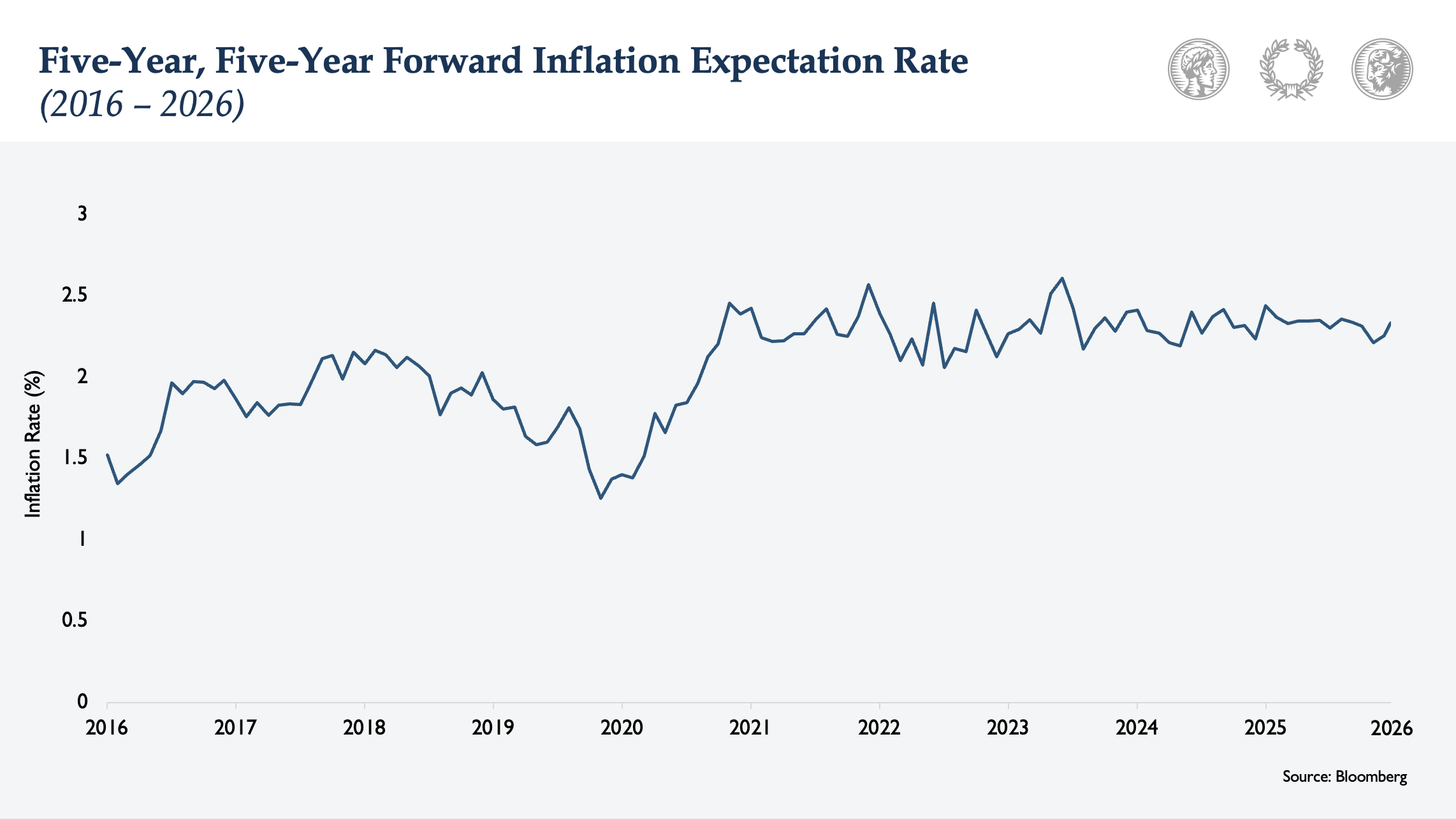

Long term inflation expectations remain relatively well anchored at 2.3%. The 5-Year, 5-Year forward inflation rate is the bond market's best guess at what average annual inflation will be over a five-year period, starting five years from now. It deliberately skips the near-term noise (supply shocks, energy spikes, etc.) and focuses on where inflation is expected to settle in the medium-to-long run. A 2.3% expectation suggests investors still expect inflation to normalize over time. Though not assured, this is an important signal. While near-term inflation readings may remain elevated due to oil prices, the bond market may be overestimating the persistence of these pressures.

If geopolitical tensions ease and energy prices stabilize, long-term Treasury yields could reverse to lower levels relatively quickly.

Other global developments are also contributing to upward pressure on sovereign bond yields.

In Japan, government bond yields have risen to levels not seen since the late 1990s as investors increasingly focus on the country’s long term fiscal challenges. An aging population, rising entitlement costs, higher defense spending and additional stimulus measures are all contributing to concerns about debt sustainability.

The UK faces a different set of pressures. Gilt yields have climbed as investors demand a higher political and fiscal risk premium amid growing uncertainty surrounding Labour Party leadership stability and future fiscal policy direction.

Importantly, the U.S. economy remains in a stronger position than many other developed economies. Consumer spending continues to hold up reasonably well, corporate earnings are robust and labor markets remain stable.

Takeaways for the Week

The increase in interest rates domestically is largely due to fears of the reacceleration of inflation. Long-term inflation expectations appear to remain well anchored.

Fiscal challenges in the UK and Japan are driving interest rates higher in these countries.

Disclosure

The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.