by Shawn Narancich, CFA

Executive Vice President Equity Research and Portfolio Management

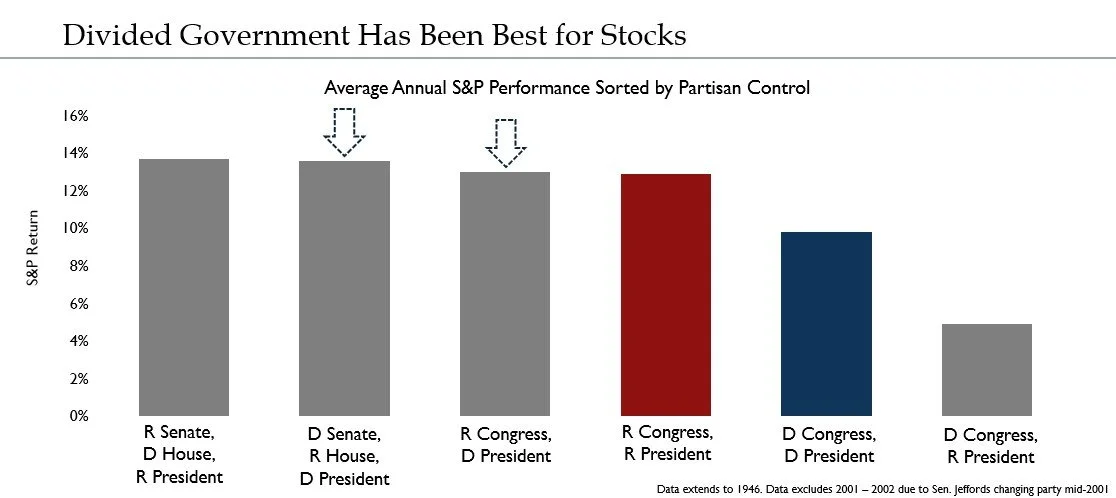

Election Postmortem

We have long observed that what matters most for investors is not the outcome of elections but rather what happens to the economy and earnings. That said, historical performance indicates that mid-term elections are clearing events - regardless of the partisan outcome. In each such event since World War II, stock prices have risen in the 12 months that followed. Although a handful of election results are still yet to be decided, the U.S. Congress appears to be headed for a split, whereby Democrats could retain voting control of the Senate while Republicans are likely to gain a slim majority in the House of Representatives. Per the chart below, an election resulting in such a “divided government” tends to be the best combination for equity investors.

Source: Strategas

Peak Inflation

Investors banking on market fireworks related to results at the ballot box got them instead from a key inflation report - the consumer-price index (CPI) came in below expectations and fell for a fourth straight month. In a sign of just how bad inflation has become, news that prices rose at a 7.7% annual rate in October was the catalyst for stocks rallying to their best daily performance in two and a half years. Though still alarmingly high, the CPI is half a percentage point lower than in September and is 1.4 percentage points below what now appears to have been this cycle’s peak of 9.1% in June. The encouraging inflation news spurred a 5.5% rally in the S&P 500 Thursday on investor expectations that the Federal Reserve’s rate hiking campaign is nearly finished.

Looking to the Fed Funds futures market, investors now anticipate our central bank will raise rates by a half percentage point in December, almost completely eliminating the possibility of a steeper 75 basis point increase. Our expectation is that inflation will continue to moderate, providing the Fed the evidence it needs to further curtail rate hikes in early 2023, before pausing them completely. In his commentary at last week’s Federal Reserve meeting, Chairman Jerome Powell acknowledged the heavy dose of interest rate increases already administered and their lagged impact on the economy, which stands to slow considerably next year amid higher credit card rates, a more than doubling of mortgage rates and rising borrowing costs for businesses.

Retailers on Deck

With 90% of blue-chip companies having now reported third quarter earnings, the S&P 500 scorecard shows that inflation has begun weighing on profit margins, with 12% higher revenues resulting in just 2% bottom line growth. Earnings growth has slowed to a crawl and would have been negative in the quarter absent the stellar performance of energy companies benefitting from robust oil and gas prices.

Retailers will round out the reporting season over the next week two weeks. The COVID-19 pandemic that kept manufacturing constrained and created logistical problems at U.S. ports resulted in a backlog of inventory that finally found its way to store shelves in 2022. General merchandisers such as Target and Walmart now have the inventory they previously lacked but face the challenge of consumer purchasing power compromised by high inflation at a time when spending has shifted to experiences such as travel and eating out. Accordingly, unit sales in categories such as full-price apparel and home furnishings are stagnating. Supporting this notion is the National Retail Federation’s estimate that holiday sales this year will rise by 6-to-8%, down from 13.8% last year and in line with current rates of inflation. Select retailers and apparel/footwear marketers such as Nike have had to take write-downs and may have to do so again amid elevated levels of inventory. Our traditional retailing exposure on behalf of clients is focused on the home improvement and off-price categories less susceptible to retail mark-downs and margin pressure.

Takeaways for the Week

Mid-term elections have likely resulted in a divided government, historically favorable for stocks

Equities and bonds rallied on better than expected inflation news