by Brad Houle, CFA

Executive Vice President

As investors digested news of the Federal Reserve's plan to unwind its balance sheet starting in October, both interest rates and equity markets remained unchanged for the week.

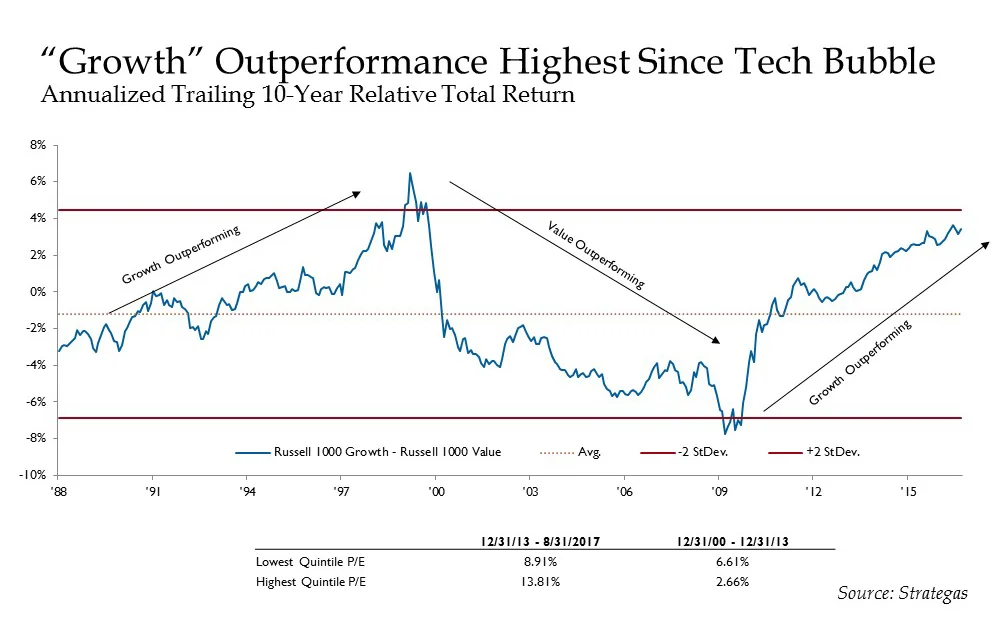

With growth investing outperforming value investing over the last decade, there has been discussion in the financial press about the death of value investing. Growth investing is defined as investing in companies with growth that is above average and these companies generally have valuation metrics that could be characterized as expensive. By contrast, value investing is purchasing stocks that appear “cheap” relative to their growth prospects. Historically over the long term, value stocks have outperformed growth stocks and experienced less volatility. Why value has a tendency to outperform over long periods of time is not a simple explanation. Investors have a tendency to overestimate the attributes of companies that exhibit growth characteristics and underestimate the prospect of companies that are considered cheap.

One of the factors that has led to the recent outperformance of growth over value has been the pace of expansion of the U.S. economy following the financial crisis. This growth stage of the economy is in its ninth year, which is both good and bad news. It’s good because the economy is still expanding and there is not a recession in sight. The bad news is that the expansion has been so slow, which has been a headwind for corporate earnings growth. This, along with tepid growth abroad and a strong dollar, has limited corporate earnings growth … until recently. As a result, investors have been willing to pay up for companies exhibiting the greatest promise for growth … with virtually no concern for valuation. This had led to narrow markets whereby a significant portion of stock market returns come from just a handful of stocks. For example, the “FANG” stocks (i.e., Facebook, Amazon, Netflix and Google) have been significant contributors to market performance and are classic growth companies.

Contributing to the growth stock and FANG outperformance has been increasing cash flow toward index funds of late. Stock market indices are capitalization-weighted, which refers to the largest companies having the greatest weighting in the index. Therefore, index funds seek to replicate stock market indices, such as the S&P 500. If money is invested into these funds, the fund manager buys more of the index, regardless of the investment merits of the individual stocks within the index. The largest stocks in the indices then have more demand, which in turn drives their prices higher … and it becomes a self-reinforcing circle.

Growth has outperformed value for the last 10 years, as is depicted in the chart above. This extended period of outperformance of value over growth is two standard deviations above the mean. Said differently, 95 percent of the time, growth does not outperform value in a long time horizon, so we anticipate that the reign of growth stocks will eventually come to an end.

Takeaways for the Week

Growth and value stocks can have extended periods of outperformance for underperformance. Over the long term, value stocks tend to outperform growth stocks

In terms of both duration and magnitude, this cycle of growth stocks outperforming value stocks is getting long in the tooth