Northwest NewsChannel 8’s Joe Smith talks with Mark Kralj, principal, about how trends in economic data seem to be improving, not deteriorating. How consumers feel about the economy is subjective, but there are indications that home ownership and retail sales are growing. A recent report from the Federal Reserve indicates that Oregon is one of three states anticipating growth greater than 4.5 percent in the next six months. Click here to view the news story.

Northwest NewsChannel 8’s Joe Smith talks with Mark Kralj, principal, about how trends in economic data seem to be improving, not deteriorating. How consumers feel about the economy is subjective, but there are indications that home ownership and retail sales are growing. A recent report from the Federal Reserve indicates that Oregon is one of three states anticipating growth greater than 4.5 percent in the next six months. Click here to view the news story.

Weekly Market Makers - Week Ending 11/2/12

by Shawn Narancich, CFA

Vice President of Research

by Shawn Narancich, CFA

Vice President of Research

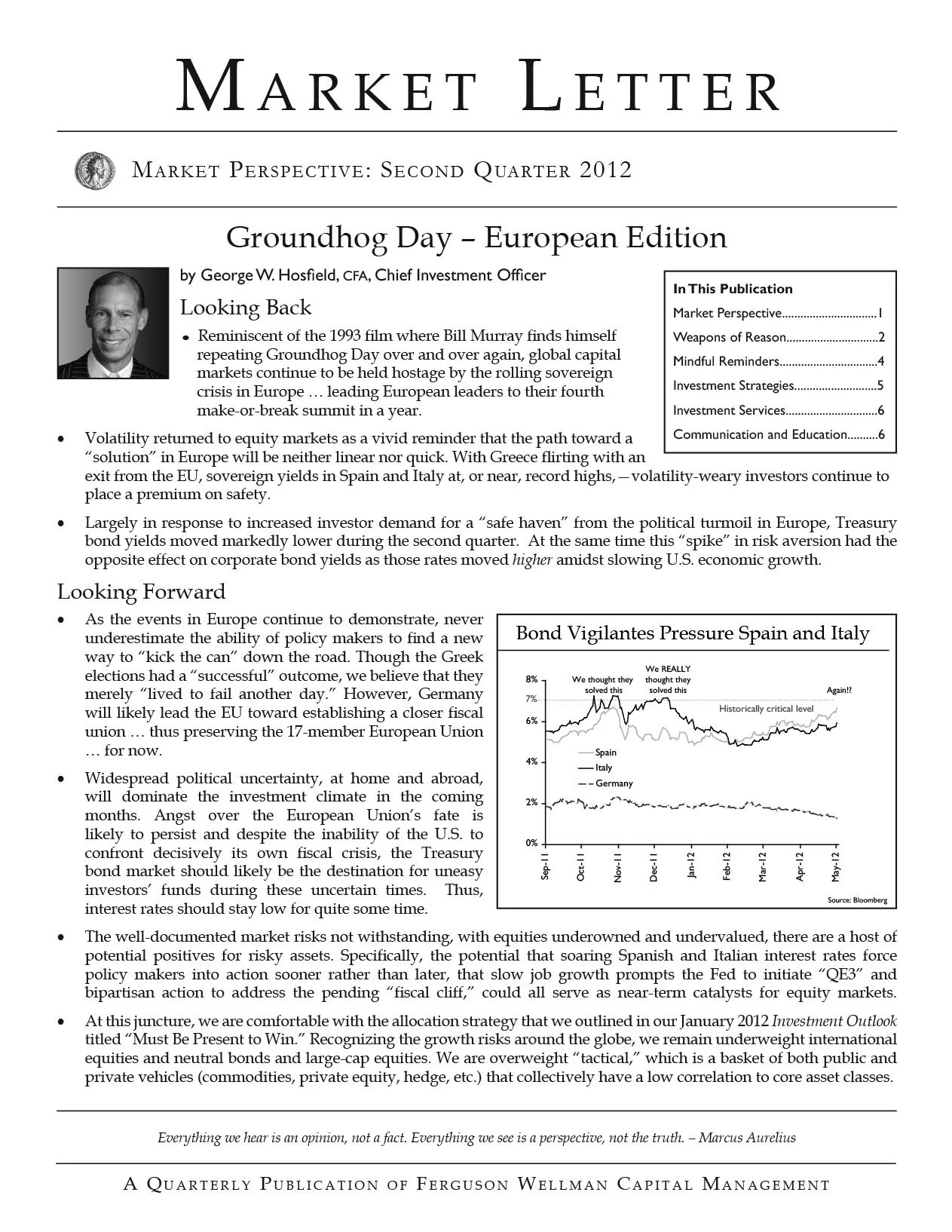

A Perfect Storm?

Hurricane Sandy left investors with idle stock screens this Monday and Tuesday as the New York Stock Exchange closed for two consecutive days—the first time that weather has done so since 1888. The loss of life and property is sobering. Our collective thoughts and prayers go out to those affected by this killer storm, which left traders and media commentators to speculate about its economic and company specific impacts. Home improvement retailers Lowe’s and Home Depot, United Rentals and pump maker Pentair were among the winners when trading resumed Wednesday. Stocks succumbed to a late Friday sell-off that left the major indexes largely unchanged for the week, with benchmark Treasuries rallying modestly.

Our best guess is that Sandy will negatively impact fourth quarter GDP, but that a massive rebuilding effort in the nation’s most densely populated corridor will result in somewhat faster economic growth early next year. Insurable losses, excluding flood damage backstopped by the federal government, are estimated to be as high as $20 billion. Catastrophic claims will ding the near-term earnings of insurers like Allstate and Chubb, as well as their reinsurance partners, but the more important question for investors is whether Sandy will precipitate the kind of rate hikes that have historically enabled property and casualty insurers to exchange near-term pain for long-term gain. Ironically, both Allstate and Chubb recently reported better-than-expected earnings, with both citing benign claims activity.

Silver Linings

Despite the hurricane, the U.S. government hewed to its plan of releasing the October payroll report as originally planned. The numbers out Friday were better than expected, with net job creation totaling 171,000 and the previous two months’ job tally being upwardly revised by a cumulative 84,000 jobs. Service sectors such as retail and healthcare were notable contributors, and manufacturing jobs rebounded. The headline jobs number was encouraging, but an uptick in unemployment to a 7.9 percent rate coupled with an underemployment rate that remains near 15 percent are stark reminders of how just how slow the labor market recovery has been. Third quarter productivity gains of 1.9 percent confirm the job market weakness, portraying a private sector that favors squeezing more output from its existing employees to hiring anew. Because unemployment remains high, workers have little leverage to demand higher wages and, as a result, unit labor costs are falling. So while revenue gains are hard to come by at this point of the economic cycle, productivity is helping buoy corporate America’s bottom line.

The Late Innings of Earnings Season

Meanwhile, earnings season rolled on. Notable misses came from oil giants ExxonMobil and Chevron, both companies displaying continued declines in petroleum production exacerbated by cyclically low natural gas prices domestically. On the flip side, automakers GM and Ford reported surprisingly good numbers in light of the losses they continue to incur in Europe. Capacity there is being curtailed, but cutting jobs in Europe is a process, not an event.

Our Takeaways from the Week

- Hurricane Sandy is exacting a substantial human and economic toll, but a resilient U.S. economy will likely recover lost output longer term

- A surprisingly poor earnings season is beginning to wind down

Norris Discusses the Threat of Hurricane Sandy

Northwest NewsChannel 8’s Joe Smith talks with Jason Norris, CFA, senior vice president of research, about the NYSE and NASDAQ closing for Hurricane Sandy.

He also speculates how the economic impact the super storm might affect the final days of the election. Click here to view.

Northwest NewsChannel 8’s Joe Smith talks with Jason Norris, CFA, senior vice president of research, about the NYSE and NASDAQ closing for Hurricane Sandy.

He also speculates how the economic impact the super storm might affect the final days of the election. Click here to view.

Weekly Market Makers - Week Ending 10/26/12

by Shawn Narancich, CFA

Vice President of Research

More Questions than Answers

Evidence of business malaise and a maturing business cycle continued to pile up in week three of the third quarter earnings season, with stocks succumbing to questions about peak sales and profit margins. For corporate executives, discretion is proving to be the better part of valor. Hesitancy to provide outlooks for 2013 reflects a European recession, slowing growth in China, and approaching fiscal headwinds that threaten to weaken a U.S. economy already flying at close to stall speed. Against this backdrop, earnings estimates and stock prices are falling. Benchmark Treasuries rallied modestly as large cap U.S. stocks fell 1.5 percent.

Hand in Glove

An initial read of 2 percent domestic growth for third quarter GDP provided apt context within which to consider the earnings of Caterpillar, DuPont, 3M and chipmaker Broadcom— all cyclical companies that told investors to reduce their fourth quarter profit expectations. Corroborating the weakness in machinery, chemical and semiconductor sales seen anecdotally in corporate America, the Commerce Department reported today that a decline in capital spending detracted from third quarter economic output. The irony of 10 percent growth in government spending lending a boost to third quarter GDP ahead of the looming fiscal cliff failed to give investors much confidence in the economy’s ongoing durability. Exports also detracted from GDP, confirming the slowdown in global trade. A bright spot is housing, which stands out for the contribution it is once again making to the GDP equation.

Exceptions to Every Rule

In a slow-growing economy exhibiting late cycle characteristics, the rare company reporting good third quarter earnings news was amply rewarded. For such disparate companies as Peabody Coal, Procter & Gamble and Yahoo, the lift these stocks received from earnings had much more to do with company specific factors than diverging views about the macroeconomic outlook. Peabody’s investors were greeted by 13 percent gains in the stock following a rare sales beat that occurred despite shuttered mines and low coal prices, with earnings benefitting from good cost control. At Procter & Gamble, better-than-expected sales and earnings cleared a low bar set after a string of disappointing quarters in which the consumer staples stalwart has ceded market share and attracted activist investor Bill Ackman. While the latest numbers were enough to alleviate some of the pressure on top management, P&G still needs to reinvigorate its top line and pare a bloated cost structure. Yahoo’s investors finally caught a break as well, with new CEO Marissa Mayer presiding over a quarter where numbers beat low expectations despite continued lackluster display add revenue.

Halfway through third quarter earnings season, an unflattering die has been cast and expectations reduced. Next week investors will tune into to reports from automakers GM and Ford, blue chip energy producers ExxonMobil and Chevron, and a slew of utilities that may have benefitted from an unusually warm summer that boosted air conditioning demand.

Our Takeaways from the Week

- Poor third quarter earnings reports reflect a slow growth economy facing fiscal headwinds

- Limited earnings visibility has caused stocks to consolidate recent gains

2012 Q2 Market Letter

2012 Q3 Market Letter

2012 Q1 Market Letter

First Quarter 2012 – Outlook for 2012 by George Hosfield, Fixed Income by Marc Fovinci, Municipal Bonds by Deidra Krys-Rusoff, REITs by Ralph Cole, Dividend Value by Jason Norris, Strategic Opportunities by Dean Dordevic, International by Ralph Cole, Alternative Investments by Dean Dordevic.

Outlook 2012

Last year was one of the most volatile periods in the history of the U.S. stock market. The Japanese earthquake and tsunami, a festering European debt crisis and dysfunctional U.S. politics weighed on consumer, business and investor sentiment in 2011—creating economic and market headwinds. Having endured a decade of boom and bust cycles in technology, real estate and commodities—U.S. investors are fatigued by a roller coaster stock market that has made little forward progress.

2011 Annual Report

2011 Q3 Market Letter

Third Quarter 2011 – Looking Back and Forward by George Hosfield, “China Derailed” by Dean Dordevic, Mindful Reminders by Mary Faulkner, Investment Strategies: Large Cap Div Val by Jason Norris, It’s Never Too Early to Start Tax Planning by Mark Kralj and New Look and Functionality for Our Website by Natalie Miller and Shawn Swagerty.

2011 Q2 Market Letter

2011 Market Letter Q1

Outlook 2011

2010 drew to a close with fears of a double-dip recession abating and economic data revealing that the global expansion was intact and gaining momentum. After a mid-year slowdown, the preponderance of economic indicators now point toward a modest reacceleration in domestic growth. For all that was written about the “new normal,” last year looked surprisingly like the “old normal.” Looking forward, the extension of Bush-era tax cuts suggests that the pace of activity will likely accelerate in the first half of 2011 and a second round of quantitative easing (“QE2”) renders a “double dip” highly unlikely. In our view the cyclical equity bull market is not yet over.

2011 Q1 Market Letter

First Quarter 2011 – Looking Back and Looking Forward by George Hosfield, “Rough Rice II: Fat Tails Wag the Dog” by Dean Dordevic, Mindful Reminders by Mary Faulkner, Municipal Bonds by Deidra Krys-Rusoff, Client Balance Sheet by Nathan Ayotte, Delivering our Investment Outlook: Events and Videos by Natalie Miller.

2010 Annual Report

2010 Q3 Market Letter

Third Quarter 2010 – Market Outlook by George Hosfield, “QE2 and the Square Root Redux” by Dean Dordevic, Year-End Tax Changes, Longevity and Continuity piece on Luz Garcia, Kathi Kimes and Kerrie Young.

2010 Q2 Market Letter

Outlook 2010

What a difference a year makes. After one of the worst years in history for investors, 2009 brought above-average returns across all equity styles. Aided by unprecedented monetary and fiscal stimulus, credit markets thawed and investors’ risk tolerance returned. Like the emergency room patient who doctors stabilize before nearly losing to anaphylactic shock, stocks rose from what felt like the dead in March, climbing a wall of worry to recoup roughly half of the damage done since the highs of 2007.

2010 Q1 Market Letter

First Quarter 2010 – “’Gray’ Matters” by Dean Dordevic, Community & Civic Service, The Value of Planning.