by Shawn Narancich, CFA

Vice President of Research

by Shawn Narancich, CFA

Vice President of Research

More Questions than Answers

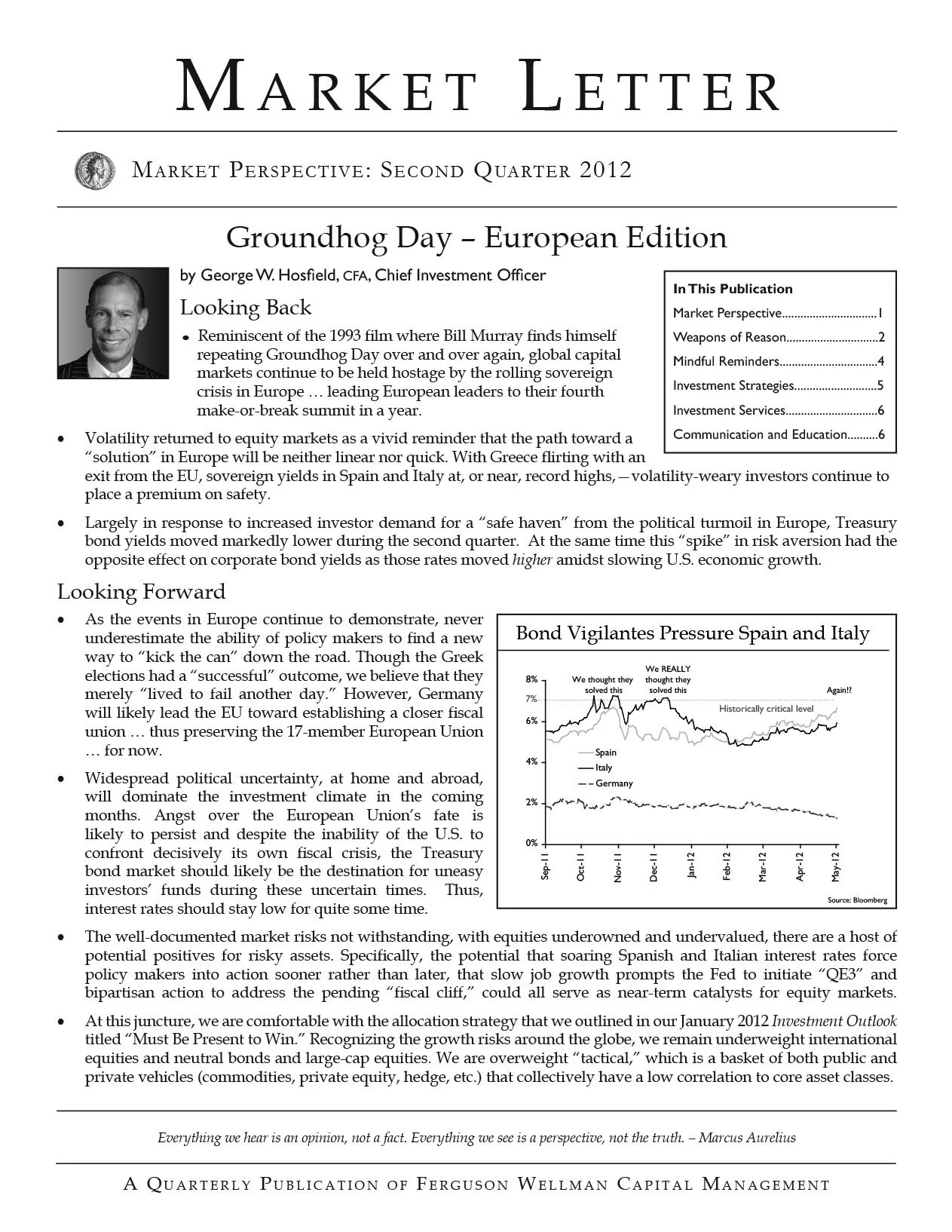

Evidence of business malaise and a maturing business cycle continued to pile up in week three of the third quarter earnings season, with stocks succumbing to questions about peak sales and profit margins. For corporate executives, discretion is proving to be the better part of valor. Hesitancy to provide outlooks for 2013 reflects a European recession, slowing growth in China, and approaching fiscal headwinds that threaten to weaken a U.S. economy already flying at close to stall speed. Against this backdrop, earnings estimates and stock prices are falling. Benchmark Treasuries rallied modestly as large cap U.S. stocks fell 1.5 percent.

Hand in Glove

An initial read of 2 percent domestic growth for third quarter GDP provided apt context within which to consider the earnings of Caterpillar, DuPont, 3M and chipmaker Broadcom— all cyclical companies that told investors to reduce their fourth quarter profit expectations. Corroborating the weakness in machinery, chemical and semiconductor sales seen anecdotally in corporate America, the Commerce Department reported today that a decline in capital spending detracted from third quarter economic output. The irony of 10 percent growth in government spending lending a boost to third quarter GDP ahead of the looming fiscal cliff failed to give investors much confidence in the economy’s ongoing durability. Exports also detracted from GDP, confirming the slowdown in global trade. A bright spot is housing, which stands out for the contribution it is once again making to the GDP equation.

Exceptions to Every Rule

In a slow-growing economy exhibiting late cycle characteristics, the rare company reporting good third quarter earnings news was amply rewarded. For such disparate companies as Peabody Coal, Procter & Gamble and Yahoo, the lift these stocks received from earnings had much more to do with company specific factors than diverging views about the macroeconomic outlook. Peabody’s investors were greeted by 13 percent gains in the stock following a rare sales beat that occurred despite shuttered mines and low coal prices, with earnings benefitting from good cost control. At Procter & Gamble, better-than-expected sales and earnings cleared a low bar set after a string of disappointing quarters in which the consumer staples stalwart has ceded market share and attracted activist investor Bill Ackman. While the latest numbers were enough to alleviate some of the pressure on top management, P&G still needs to reinvigorate its top line and pare a bloated cost structure. Yahoo’s investors finally caught a break as well, with new CEO Marissa Mayer presiding over a quarter where numbers beat low expectations despite continued lackluster display add revenue.

Halfway through third quarter earnings season, an unflattering die has been cast and expectations reduced. Next week investors will tune into to reports from automakers GM and Ford, blue chip energy producers ExxonMobil and Chevron, and a slew of utilities that may have benefitted from an unusually warm summer that boosted air conditioning demand.

Our Takeaways from the Week

- Poor third quarter earnings reports reflect a slow growth economy facing fiscal headwinds

- Limited earnings visibility has caused stocks to consolidate recent gains