by Jason Norris, CFA

Director

Equity Research and Portfolio Management

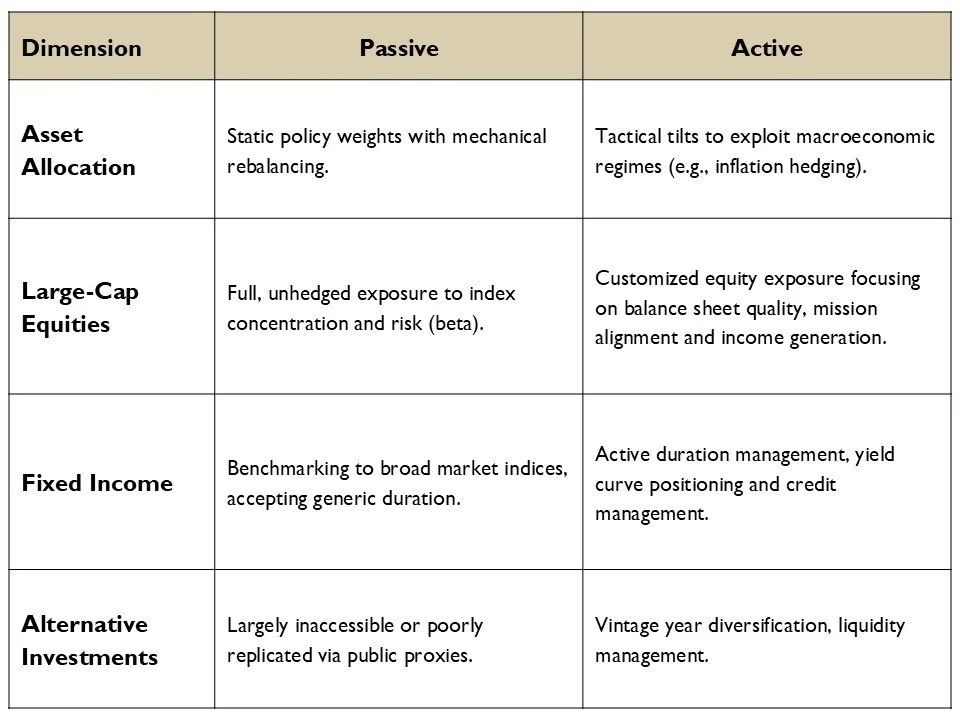

For institutional trustees, investment committee members and board governors, the active-versus-passive debate is often framed through a narrow lens: security selection and manager alpha. However, focusing solely on whether an investment manager can outperform an index obscures the more critical fiduciary responsibility, and this is total portfolio oversight. At the institutional level, active management is properly understood not as a return-chasing exercise, but as the deliberate, dynamic governance of risk, liquidity, cash flow and, importantly, asset allocation.

The Limits of Indexation in Institutional Frameworks

Passive management offers some structural benefits: low implementation costs, high liquidity and predictable market replication. However, a purely passive posture introduces systemic vulnerabilities for pools of capital governed by specific spending policies or long-term liabilities:

Market-Weighted Concentration Risk: Passive indices are generally weighted by capitalization and therefore they may increase exposure to potentially overvalued sectors and individual mega-cap constituents as their market values grow, without any acknowledgement of risk. For instance, today the top three holdings of the S&P 500 combine to 20% of the entire index.

Liquidity Concerns: Index funds are generally price takers, obliged to buy and sell regardless of valuation or macro-level dislocations

Inherent Benchmarking Constraints: For endowments, foundations and pensions, the true benchmark is the institution's required rate of return (spending policy + inflation + fees). A static passive portfolio cannot easily adapt when capital market assumptions change.

Large-Cap Security Selection as a Risk and Customization Tool

A common misconception among institutional committees is that the benefit of active security selection in large-cap equities is obsolete due to market efficiency. While generating gross outperformance is never guaranteed, active management often provides downside protection and precise portfolio customization.

In a cap-weighted index, investors are forced to own every company regardless of leverage, volatility or institutional alignment. Active security selection allows boards to tailor their core equity exposure to specific institutional objectives. For example, the Ferguson Wellman Dividend Value investment strategy has the following attributes:

Targeted Dividend and Income Focus: For institutions heavily reliant on steady distributions to meet spending mandates, passive indices generally offer a standardized yield, not customized to the specific client. Active large-cap selection can often tilt the portfolio toward high-quality, dividend-paying companies with robust free cash flow generation. This prioritizes organic income over the potential of forced asset liquidations during market downturns.

Alignment with Institutional Values and Beliefs: Boards frequently oversee pools of capital tied to specific missions, such as universities, or religious organizations. Passive index funds are blunt instruments that include companies that conflict with those values. Active mandates allow institutions to exclude holdings that conflict with organizational values while maintaining diversification.

Managed Volatility: Committees can mandate active strategies designed to mitigate broad market volatility. By intentionally selecting low-beta or high-quality factors, active managers can design portfolios that aim to participate in a majority of the market upside while limiting market downside. For an institution relying on steady distributions, smoothing this volatility curve preserves capital that compounds faster from a higher base.

Asset Allocation as Institutional Governance

Fiduciary duty requires boards to look beyond simple manager selection and focus on asset allocation, which empirically drives the vast majority of portfolio return and volatility. True active institutional management manifests at the total-portfolio level through several critical mechanisms:

Conclusion

At first glance, institutional boards might view passive management as the most cost-effective option, but active management can provide a framework for comprehensive risk governance and portfolio management beyond simply tracking benchmark returns. An active management methodology allows trustees to better align their investment strategy with the institution’s long-term mission and financial sustainability.

Conversation Starters for Nonprofit Professionals and Board Members

Are passive management fees always the lowest cost option?

Passive management might appear to be a low-cost option at first glance, however, when considering investment options, be aware of all layers of fees that you or your organization may be paying outside of the typical investment vehicle and the investment manager/consultant fees. These other fees might include mutual fund and/or ETF fees, management fees, trading costs and consultant fees, depending on how the management of investments is structured. Fees are not inherently bad as long as trustees understand what they are and what they pay for.

What is the value of using both passive and active management?

Trustees should review the objectives, risk appetite, cash flow needs and any other preferences or restrictions that might impact their investments. This will give them a more holistic view rather than just focusing on the low-cost option.

Does active management have a low probability of outperforming the market long-term?Active management across different asset classes have different probabilities to outperform. Perhaps more important is the overall portfolio performance and management.

Disclosure: The views expressed represent the opinion of Ferguson Wellman. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Statements of future expectations, estimates, projections and other forward-looking statements are based on available information and Ferguson Wellman’s views as of the time of these statements. Past performance may not be indicative of future results. Ferguson Wellman, Octavia Group and West Bearing do not provide tax, legal, insurance or medical advice. This material has been prepared for general educational purposes only and not as a substitute for qualified counsel who can determine how this information applies to you. We believe the information provided is from reliable sources but should not be assumed accurate or complete.

Please see additional disclosures.